Marketing Managers

Executive Summary

In this comprehensive national rental demand report, we outline significant changes in unique leads per property across Canada. The data presented here is the largest data-backed analysis of rental market demand in Canada using aggregate ILS data (over 20 rental listing sites).

The data included in the Rentsync National Rental Demand Report can be used to compare and contrast demand and lead volume for the properties you manage within a given city and will allow you to make more sound decisions on marketing and advertising.

As you observe demand and unique lead volume percentage, it's possible to measure this against your own metrics, and see whether you are in line with current industry trends, and if not, how to pivot your strategies as a result.

Methodology

In order to present this data, Rentsync has determined three key calculations for each area of the report, they are as follows:

Demand Score: Our demand score is rated out of 10 (with 10 being the highest score a city can receive), and is calculated based on unique leads per property, per city, and compared against benchmark data.

For example: If Surrey, BC received a demand score of 10 this month, versus 9.6 last month. Therefore, Surrey experienced an increase in its demand score by .3 this month.

Demand Percentage (% +/-): This is determined according to the year-over-year (YOY) or month-over-month (MOM) increase or decrease in unique leads per property.

For example: The month-over-month unique leads per property in Surrey, ON went up 5% in March versus February. In March 2022, the year-over-year Demand Score in Surrey, ON went up 4.0 points based on an increase of 71% unique leads per property compared to December 2020.

Position: The position is determined by unique leads per property, with cities that have at least *20 properties or more. The position will vary depending on demand.

For example: This month, Surrey, BC remained at the top spot on the Top 40 Canadian Cities in Demand. Year-over-year Surrey, BC continued to remain in the 1 spot since last year.

*The following report provides month-over-month rental listing data for March 2022 versus February 2022, as well as a year-over-year comparison from March 2022 versus March 2021. It also outlines the month-over-month and year-over-year trends in primary, secondary, and tertiary markets.

Key Takeaways:

Month-over-month (M/M): March saw an overall expansion of market conditions with the supply of available properties increasing by +2.2%, and the number of prospects increasing by +29%. This resulted in average leads per property increasing and becoming more concentrated as more renters compete for a supply of properties that are not keeping pace.

Month-Over-Month (M/M)

- Primary: Unique leads per property are up +28%

- Secondary: Unique leads per property are up +23%

- Tertiary: Unique leads per property are up +27%

*With an early spring comes an early start to the leasing season. Although February saw a slight decline in market conditions, as would be expected in the first few months of the year, March saw a strong surge in the volume of incoming inquiries. Primary markets are leading the uptake in demand and represent well over 64% of the total inquiry volume.

Year-over-year (Y/Y): Overall, in Canada, our multifamily demand score shows an increase of +84.4% in February 2022 versus February 2021. Although overall demand figures are up; both prospects and available properties are down by -37.1%, and -37.7% respectively. The loss in prospects is primarily due to the loss of Facebook marketplace as a source of property leads, while a reduction in property availability is simply a result of strong leasing activity. These conditions suggest that Canada has likely returned to its pre-covid leasing conditions, and the supply of available units continues to decrease at a higher relative rate than that of the demand for apartments. Overall, the year-over-year (March '22 vs March '21) market snapshots are as follows:

Year-Over-Year (Y/Y)

- Primary: Unique leads per property are up +135%

- Secondary: Unique leads per property are up +158%

- Tertiary: Unique leads per property are up +86%

*The year over year analysis indicates that rental demand has maintained an upward trajectory as markets stabilize and enter the annual leasing season.

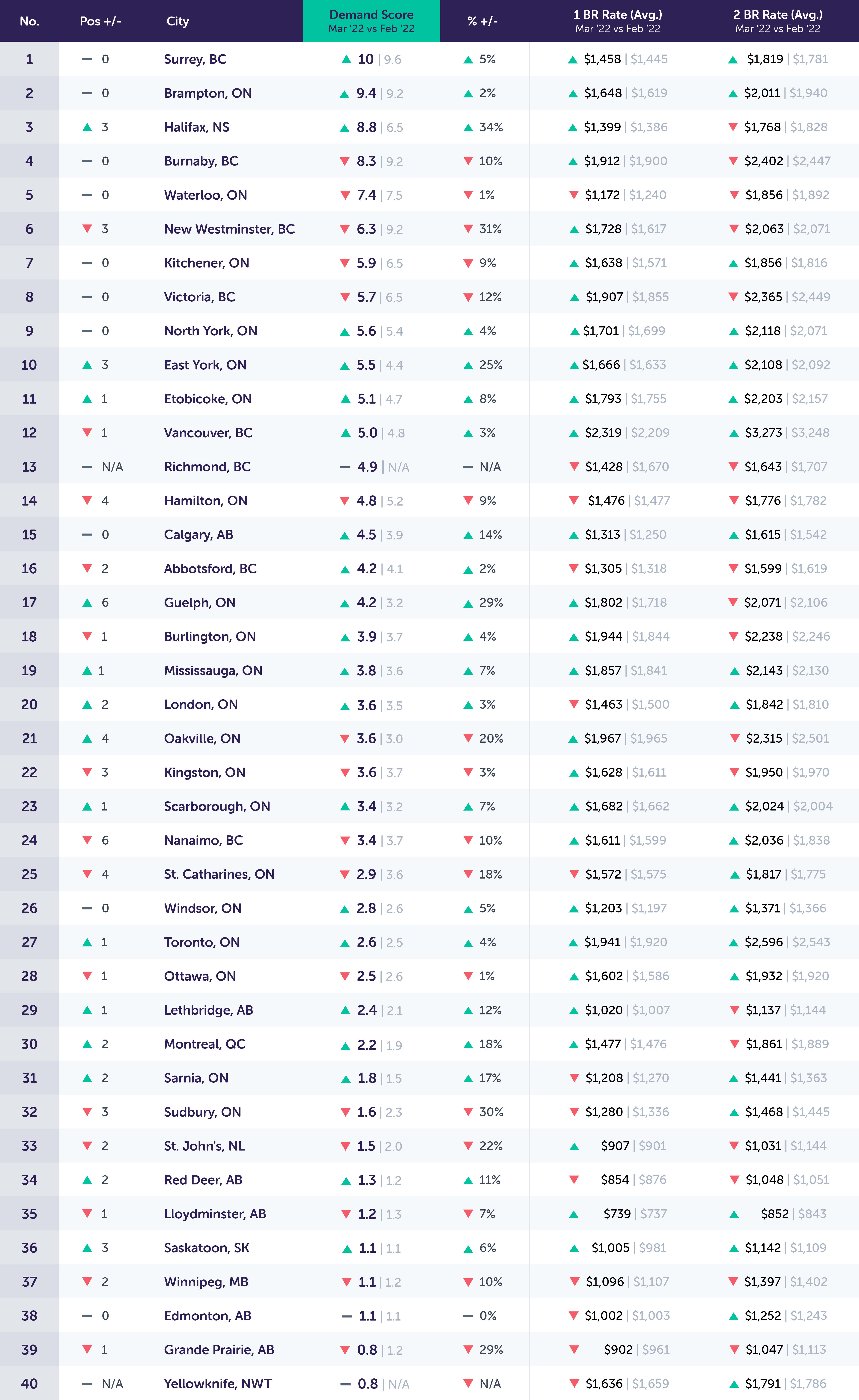

Top 40 Canadian Cities in Demand

*Demand is determined by calculating unique lead volume per property by market. Due to a decrease in available properties in the rental housing market, this report will only highlight the top 40 cities in Canada based on our threshold that requires at least 20 properties to be included in our data sample.

Notable Changes in Demand Over the Past Month

Overall, Canadian cities experienced a +29% increase in unique leads per property month-over-month (February 2022 to March 2022).

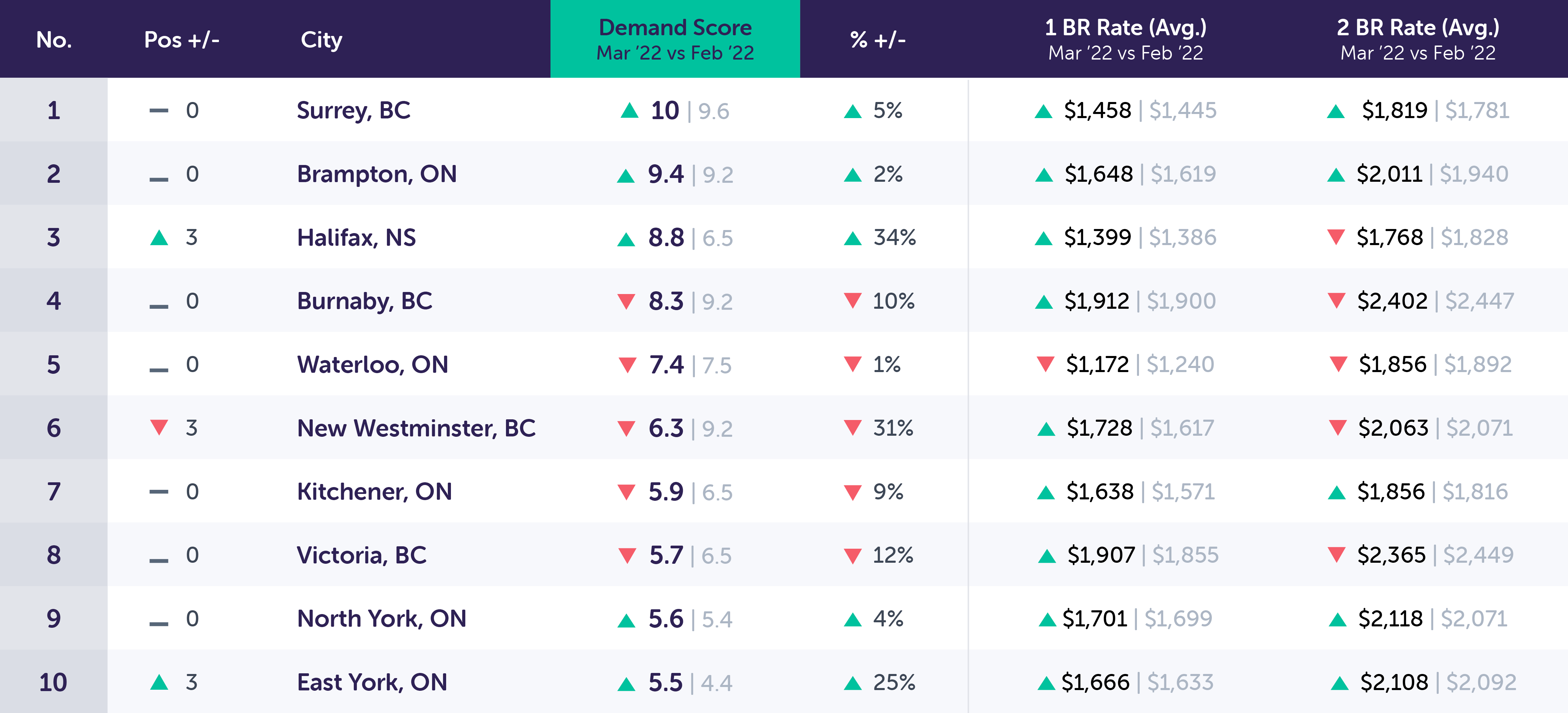

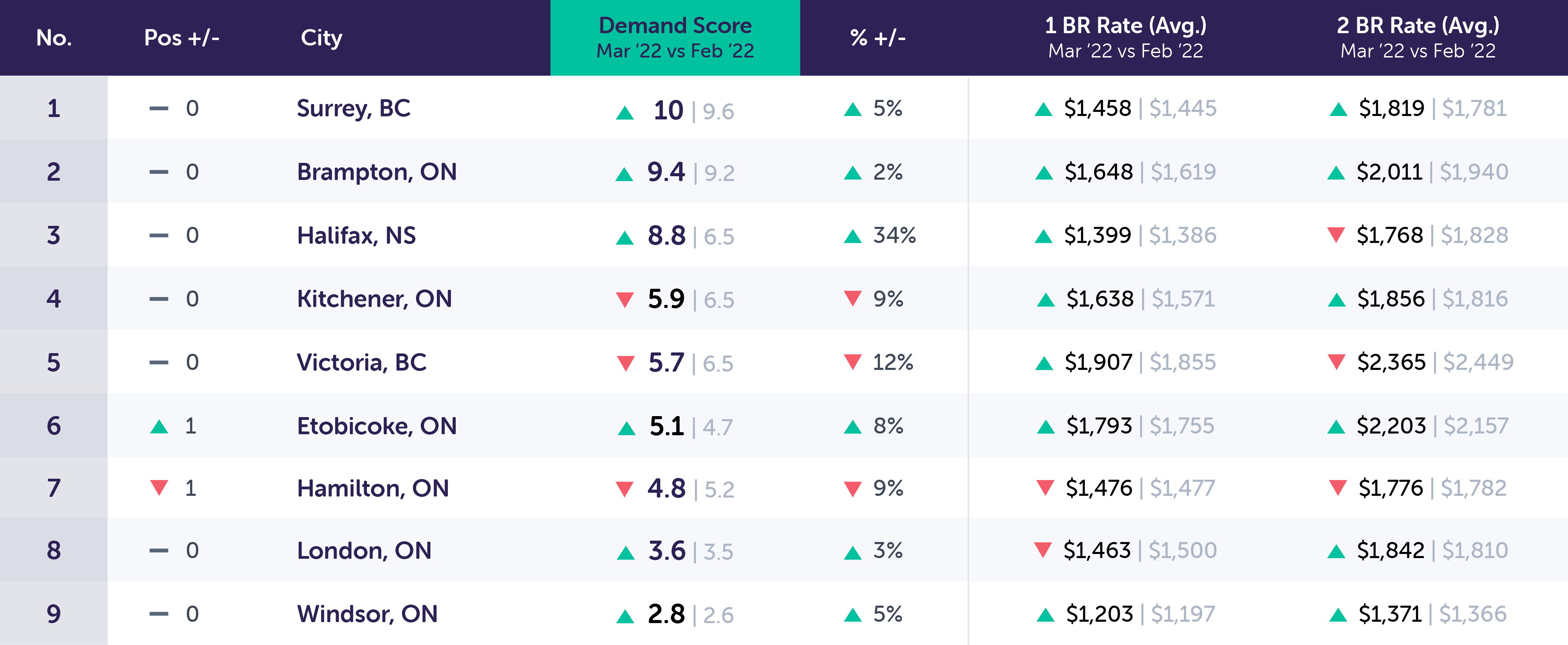

Top 10 Canadian Cities in Demand Drill Down (M/M): March 2022 vs. February 2022

Key Trends for Top 10 Canadian Cities in Demand (M/M)

*March, although on the early end of what is considered leasing season, experienced a lift in renter traffic (Following the blip experienced in February with sluggish demand and property availability). The top 10 markets are highly reflective of what is being seen across Canada, with primary and tertiary markets growing, and secondary markets experiencing a mix of more moderate growth if not slight contraction in demand scores.

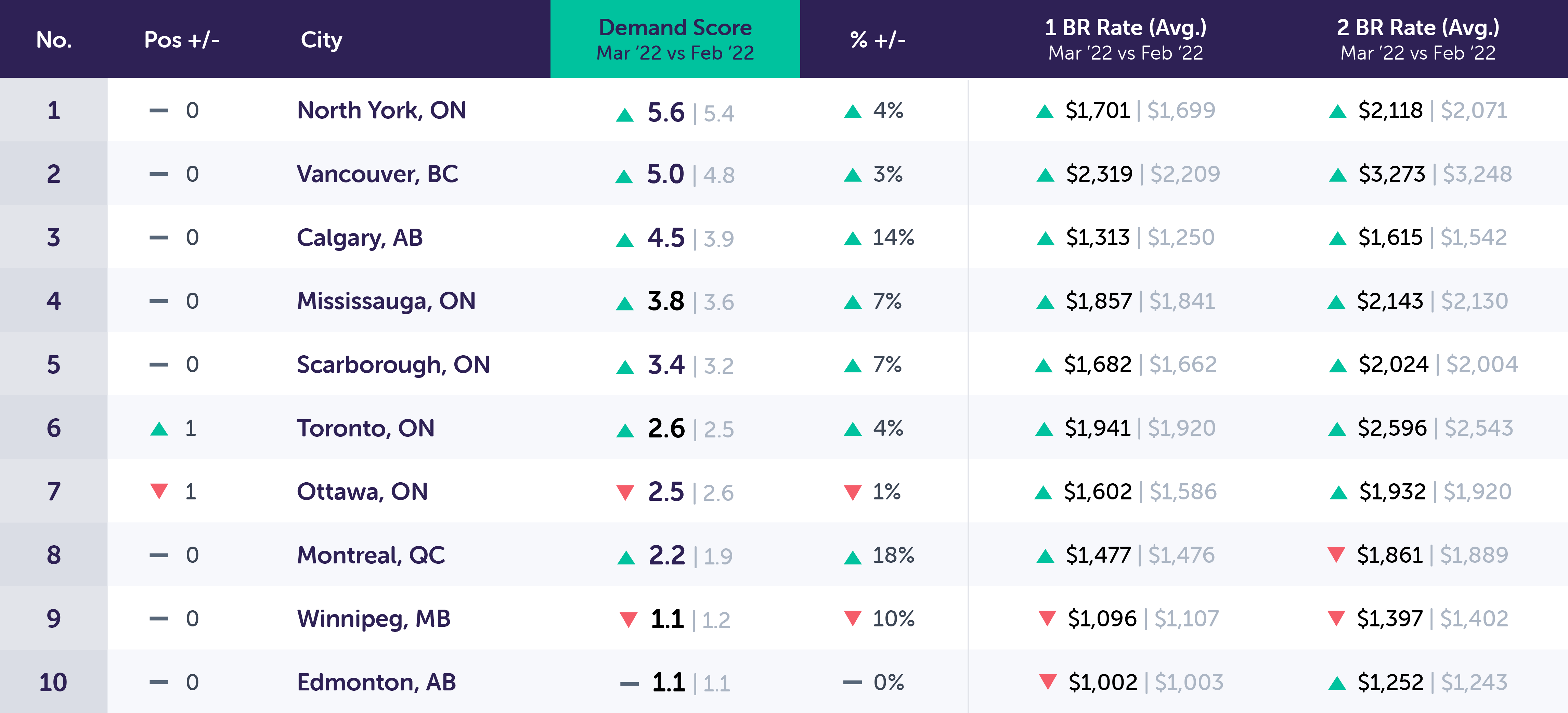

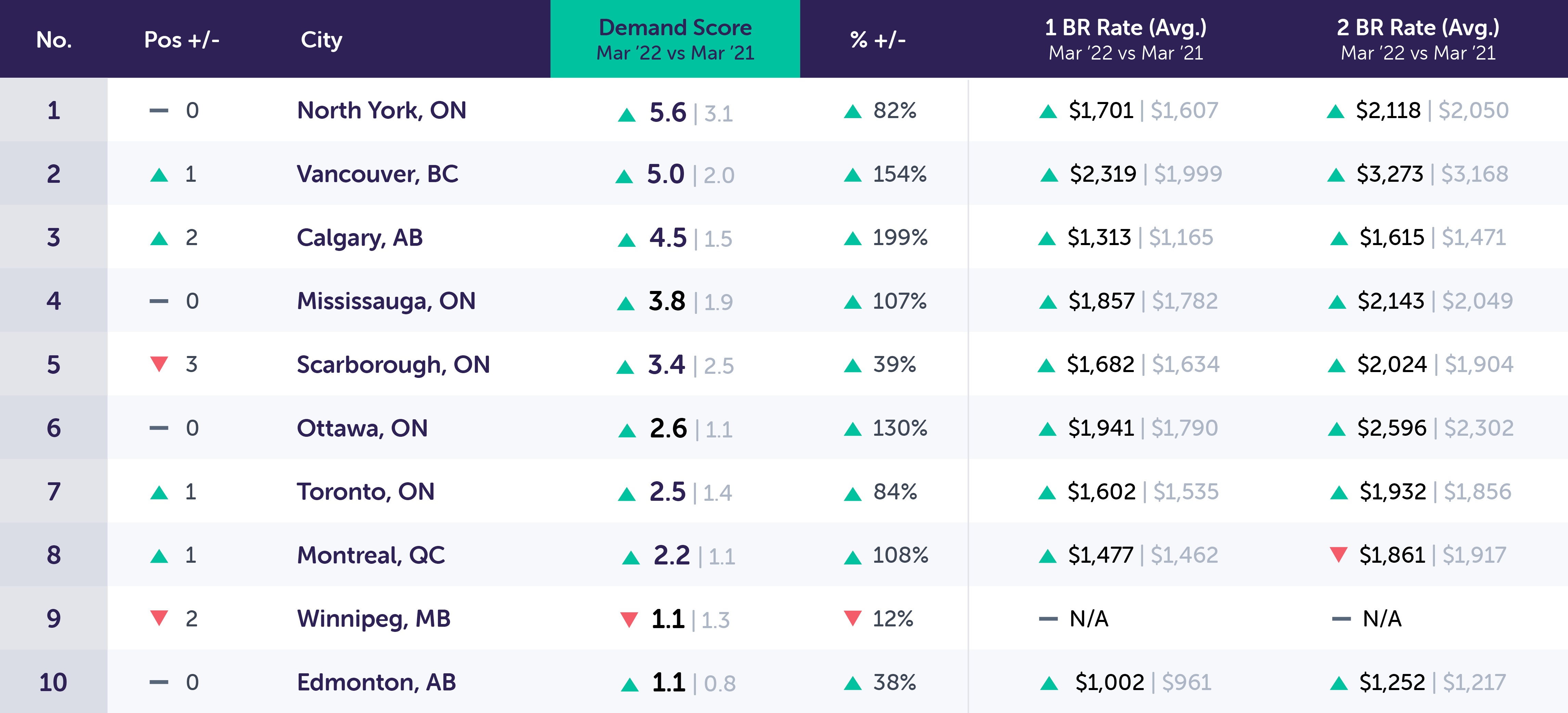

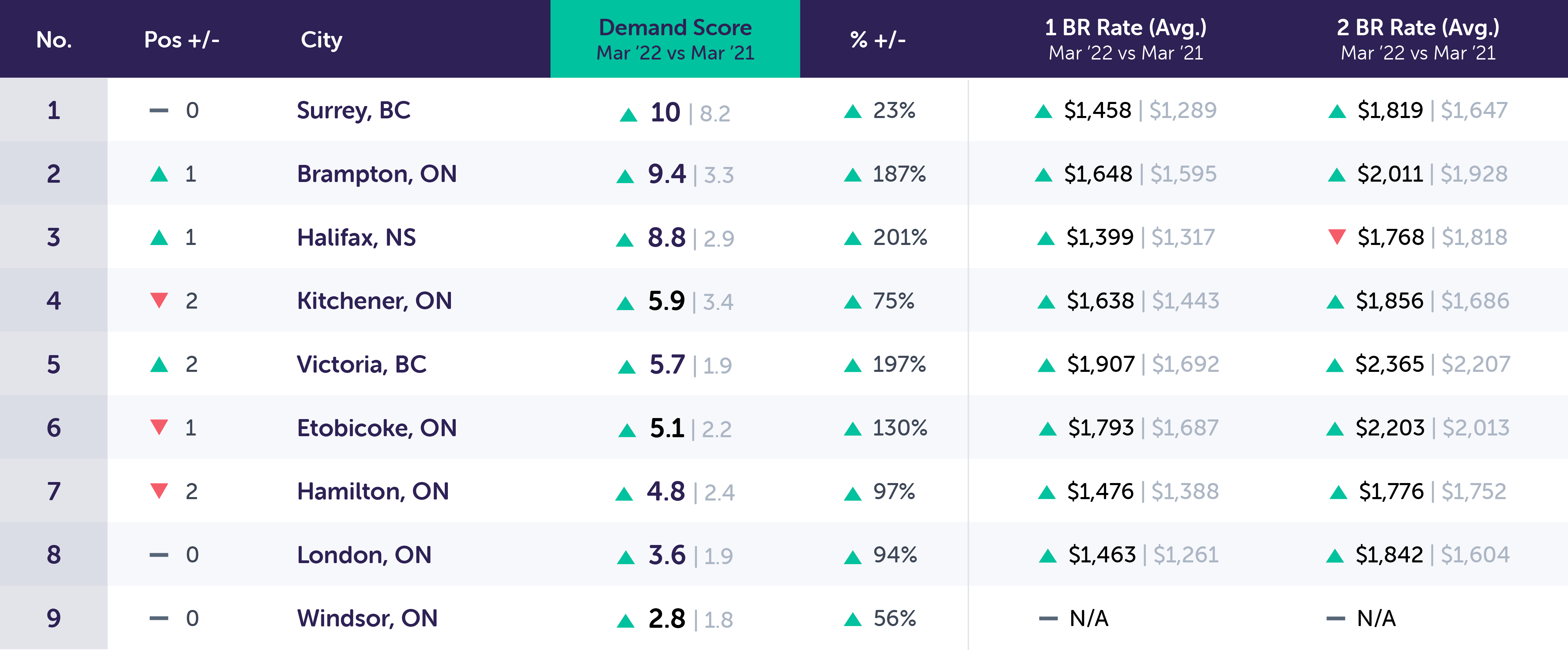

Top 10 Canadian Cities Drill Down (Y/Y): March 2022 vs. March 2021

Key Trends for the Top 10 Canadian Cities in Demand (Y/Y)

*Year over year we see the continued long-term normalization of renter traffic and inquiry volume with exaggerated growth figures and wild fluctuations in renter demand. Unlike our current monthly trends, the biggest annual gainers are secondary markets with serious growth in renter traffic and achievable rental rates. Surrey continues to top our list while also achieving the lowest overall year of year growth of +23%. Although showing more muted growth, it remains a strong prospective community for many households in the greater Vancouver area offering proximate living, at a more affordable rate. This enabled Surrey to maintain a strong inquiry volume throughout 2021, unlike many other less favourable communities which experienced a more serious rebound in 2022.

Renters have mostly returned to their preferred major markets which put a stop to the trend of urban emigration experienced throughout the last 2 years. Typically focused on smaller one-bedroom units, many are now shifting their focus to larger 2 and 3 bedroom units. Whether due to the need for at-home workspace or simply a want for more living area the rents for these units are accelerating.

Tertiary markets remain strong attractors for younger families and will continue to be in high demand as rental rates continue to grow and price many out of major housing markets.

An Analysis of Key Canadian Markets

In order to better segment our data and analyze what is happening within specific markets across Canada, we have broken down our data into 3 key market segments:

- Primary (Populations Over 600K)

- Secondary (Populations Between 600-235K)

- Tertiary (Populations Between 235-100K)

Here we will gain a deeper perspective on demand across larger populations and any movement due to the impact of COVID-19 on the rental market.

Key Takeaways:

In March, the demand posed by prospective renters outpaced the increase in available properties across all market types. As more renters continue to re-enter the rental market we are likely to see a continued increase in leads per property and heightened demand scores.

This marks a shift from the recent trend which saw a decrease of both inquiries and available properties likely resulting from a nearly total removal of Covid associated restrictions and warmer weather.

Primary Markets (Populations >600K)

Primary Market Drill Down (M/M): March 2022 vs. February 2022

Notable Changes in Primary Markets Over the Past Month

*Overall unique leads per property increased by +28% in primary markets this month.

Primary markets continue to be the strongest growers month over month with no signs of sluggishness as experienced in February. Unique leads per property are up +28% in March (compared to +1% from January to February). This is primarily attributed to the increase in prospective renters +32% likely due to the improving weather motivating many prospective renters to begin their next apartment search in advance of the summer months.

(See the year-over-year analysis below, for more perspective on demand in primary markets.)

Primary Market Drill Down (Y/Y): March 2022 vs. March 2021

Notable Changes in Primary Market Demand Over the Past Year

*Overall, year-over-year demand scores have rebounded when compared to the same time last year and have increased +135%. Unique leads per property are more compressed and are up +3.7%. Ongoing and continued reopening of major markets has also had a major impact on this strong yearly growth with many motivated to return to major markets competing for a shrinking supply of available properties.

Alongside the strong demand for apartments, we also experience growth in rental rates which suggests that not only has demand rebounded, but that market conditions have normalized and that rental rates are no longer being set based on their ability to attract renters, but are set based on current market conditions which have resulted in rents increasing across a majority of markets.

Secondary Markets (Populations ~600-235K)

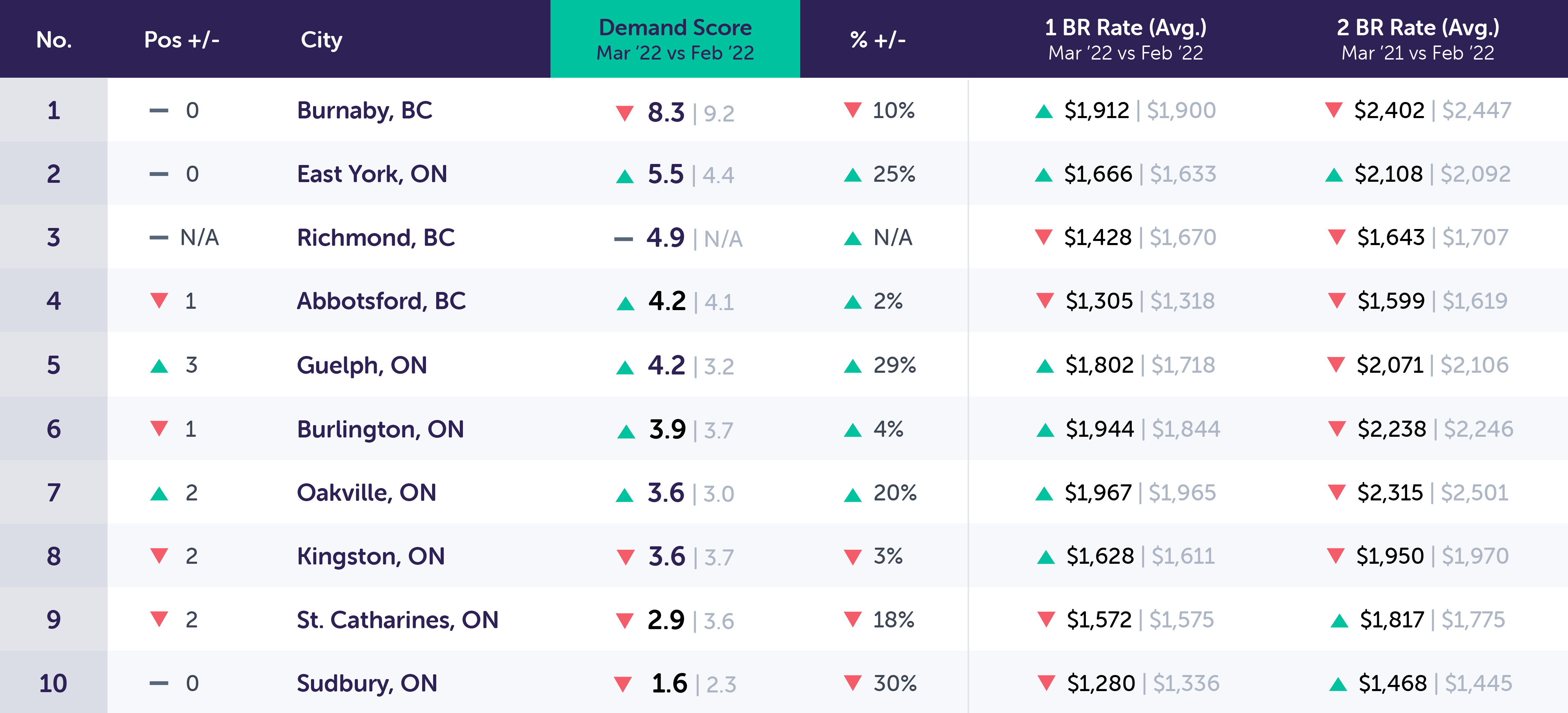

Secondary Markets Drill Down (M/M): March 2022 vs. February 2022

Notable Changes in Secondary Market Demand Over the Past Month

*Secondary markets saw an increase of +23% in demand scores, and a +25% increase in unique leads per property this month. Property availability remains relatively stable with an overall change of -1% which varies from market to market.

Rental rates which have experienced significant price fluctuations over the previous 3 months have also stabilized with an average change of +1.2% for 1-bedroom units and +0.6% for 2-bedroom units. With the return of many renters to primary markets, secondary markets struggled to maintain their appeal and began to compete on price, however, this seems to have changed as a severe imbalance between the demand by prospects and the supply of properties creates more competition amongst the available supply of rental properties. These are positive indicators leading into a leasing season which is likely to be more competitive than previous years; lending further credence to the importance of good finishes and a solid marketing plan.

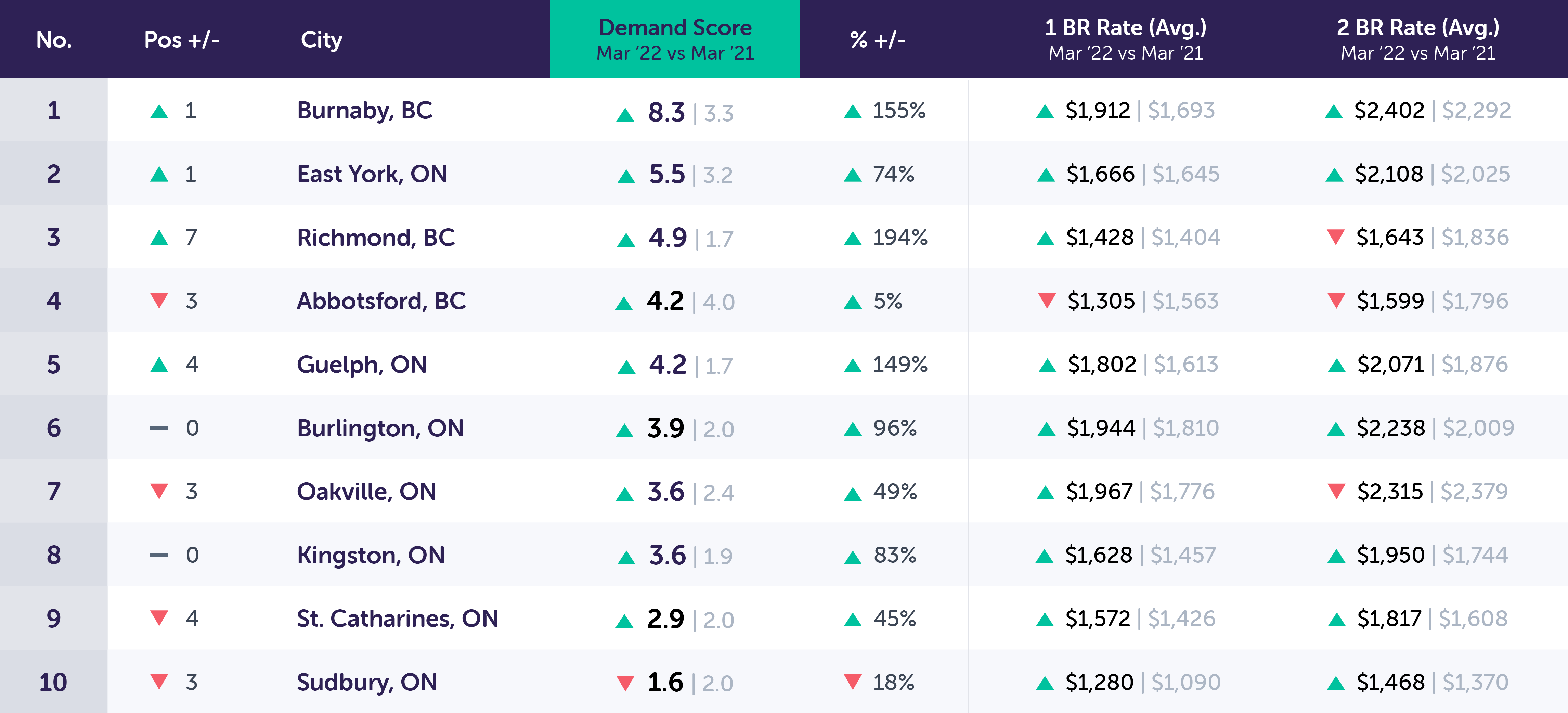

Secondary Market Drill Down (Y/Y): March 2022 vs. March 2021

Notable Changes in Secondary Market Demand Over the Past Year

*Overall, demand scores are up +158%, and unique leads per property are up +13.7% in secondary markets this year versus this time last year. The significant year-over-year increase suggests that secondary markets are the largest earners over the previous 12 months with substantial growth in unique leads per property. We see a decrease in the overall availability of properties year over year which has outpaced the decrease in rental inquiries.

Almost all markets in this segment saw an increase when compared to March of last year likely due to the more significant rise in leasing activity experienced in March of 2022. Strong rent growth is likely to continue within these communities as they prove their value to prospective renters by offering various employment opportunities, strong amenitization, and a lower cost of living.

Tertiary Markets (Populations ~235-100K)

Tertiary Markets Drill Down (M/M): March 2022 vs. February 2022

Notable Changes in Tertiary Market Demand Over the Past Month

*Unique leads per property increased by +27% this month versus last month in tertiary markets.

While February’s decline saw a slight regression, March should be seen as a sign of things to come. The warm weather brings with it a renewed interest in housing regardless of market, and while initially believed that tertiary markets would not be able to maintain their COVID achieved interest levels, they are in fact displaying signs of growth. Overall prospects increased by +29.4% month over month, which when combined with the +0.3% change in properties suggests further tightening conditions and more competition within the top end of the market.

(See the year-over-year analysis below, for more perspective on the rise in demand in tertiary markets.)

Tertiary Markets Drill Down (Y/Y): March 2022 vs. March 2021

Notable Changes in Tertiary Demand Over the Past Year

*Overall, demand scores are up in tertiary markets, increasing by +86% in March 2022 versus March 2021. Unfortunately, this does not paint the full picture as unique leads per property are down -17.8% year over year. Prospects have declined at a faster rate than available properties which has resulted in a severe reduction in average lead volume.

Although tertiary communities experienced gains throughout the pandemic in regards to increasing rental demand, much of this growth has receded indicating some of the appeals which had attracted many households has dissipated with many returning to larger communities. While rents have mostly stabilized with most markets showing strong rent growth, the actual demand for rental product is suggesting less interest.

Regardless, the overall trend of moving to smaller communities persists suggesting that moving forward there are likely to be several markets that successfully maintain this trend and become more rental-focused in the future.

Conclusion

Leasing season is upon us; whether leasing agents and marketers are ready or aware or not, the trends amongst prospective renters certainly convey that message. February experienced what should be considered a normal downturn, given seasonality in both property availability and the number of prospects, while March saw an increase in both metrics heating up the rental market.

The strong growth in rental inquiries at the head of the annual leasing season is likely indicative of what is going to be a strong leasing season. Compounded with this summer being the first in 2 years without government restrictions limiting people’s ability to move, we are likely to see strong demand and subsequently strong leasing activity moving forward. Available product is at the lowest it’s been in over 2 years which will create further pressure on the available supply of units and create conditions for greater competition amongst renters.

Much if not all of the rental stock left vacant throughout the previous 2 years has been absorbed by renters returning to primary markets. Secondary markets have similarly been able to return to stabilized conditions, however, with substantially fewer available properties than there are renters, we see the potential for significant competition by renters for the limited high-quality rental stock which remains available. And lastly, tertiary markets while similarly experiencing an influx in renter demand are lagging behind larger markets.

Moving forward we are likely to continue seeing a strong momentum of leasing activity across both primary and secondary markets, and strongly maintained rental demand across the country. While the Federal Government has enacted new measures to curb the speculative nature of Canadian real estate, these measures are unlikely to severely affect the rental industry’s trajectory in the coming months as we ramp up for greater leasing activity.

We will continue to monitor, and provide an in-depth data analysis, month-over-month, and year-over-year to provide you with the most accurate insights that can help to support your ongoing marketing and advertising strategies, especially as we navigate through these unprecedented times.