Marketing Managers

Executive Summary

In this comprehensive national rental demand report, we outline significant changes in unique leads per property across Canada. The data presented here is the largest data-backed analysis of rental market demand in Canada using aggregate ILS data (over 20 rental listing sites).

The data included in the Rentsync National Rental Demand Report can be used to compare and contrast demand and lead volume for the properties you manage within a given city and will allow you to make more sound decisions on marketing and advertising.

As you observe demand and unique lead volume percentage, it's possible to measure this against your own metrics, and see whether you are in line with current industry trends, and if not, how to pivot your strategies as a result.

Methodology

In order to present this data, Rentsync has determined three key calculations for each area of the report, they are as follows:

Demand Score: Our demand score is rated out of 10 (with 10 being the highest score a city can receive), and is calculated based on unique leads per property, per city, and compared against benchmark data.

For example: Surrey, BC received a demand score of 8.0 this month, versus 6.3 last month. Therefore, Surrey experienced an increase in its demand score by 1.7 this month.

Demand Percentage (% +/-): This is determined according to the year-over-year (YOY) or month-over-month (MOM) increase or decrease in unique leads per property.

For example: The month-over-month unique leads per property in Surrey, ON went up 28% in December versus November. In December 2021, the year-over-year Demand Score in Surrey, ON went up 2.0 points based on an increase of 34% unique leads per property compared to December 2020.

Position: The position is determined by unique leads per property, with cities that have at least *20 properties or more. The position will vary depending on demand.

For example: This month, Surrey, BC moved up 2 spots on the Top 40 Canadian Cities in Demand. Year-over-year Surrey, BC is up 1 spot since last year.

*The following report provides month-over-month ILS data for December 2021 versus November 2021, as well as a year-over-year comparison from December 2021 versus December 2020. It also outlines the month-over-month and year-over-year trends in primary, secondary, and tertiary markets.

Key Takeaways:

Month-over-month (M/M): Overall, unique leads per property from November to December increased by +18.3%. Although total unique leads dropped in the month of December by 20.4%, a normal seasonal decline, supply dropped significantly more, by 33%, resulting in leads per property to be more concentrated due to a shortage of available listings. The month-over-month market snapshots are as follows

Month-Over-Month (M/M)

-

Primary: Unique leads per property are up 21.7%

-

Secondary: Unique leads per property are up 20.6%

-

Tertiary: Unique leads per property are up 0.1%

* During this period these markets experienced a substantial decrease in available product, while actual demand or inquiries experienced a relatively lower decrease. This lower relative decrease in renter traffic has resulted in overall unique leads per property values increasing for the top cities across these individual markets.

Year-over-year (Y/Y): Overall, in Canada, unique leads per property for multifamily residential housing was up +38.5% in December 2021 versus December 2020, indicating that rental demand remains on an upwards trajectory regardless of seasonal effects or supply availability. Overall, the year-over-year (December '21 vs December '20) market snapshots are as follows:

Year-Over-Year (Y/Y)

-

Primary: Unique leads per property are up 81.1%

-

Secondary: Unique leads per property are up +120..0%

-

Tertiary: Unique leads per property are up +49.56%

*The year over year analysis indicates that rental demand has maintained an upward trajectory as markets continue to return to pre covid fundamentals and many households are increasingly willing to make housing decisions.

Top 40 Canadian Cities in Demand

*Demand is determined by calculating unique lead volume per property by market. Due to a decrease in available properties in the rental housing market, this report will only highlight the top 40 cities in Canada based on our threshold that requires at least 20 properties to be included in our data sample.

*Please note we have made improvements to our report to better serve readers looking for more in-depth rental market insights.

Notable Changes in Demand Over the Past Month

Overall, Canadian cities experienced an increase in unique leads per property month-over-month (December 2021 vs November 2021). This is likely due to rental supply shrinking by 33% in comparison to demand, which only saw a 20.5% decrease in unique leads overall for the month.

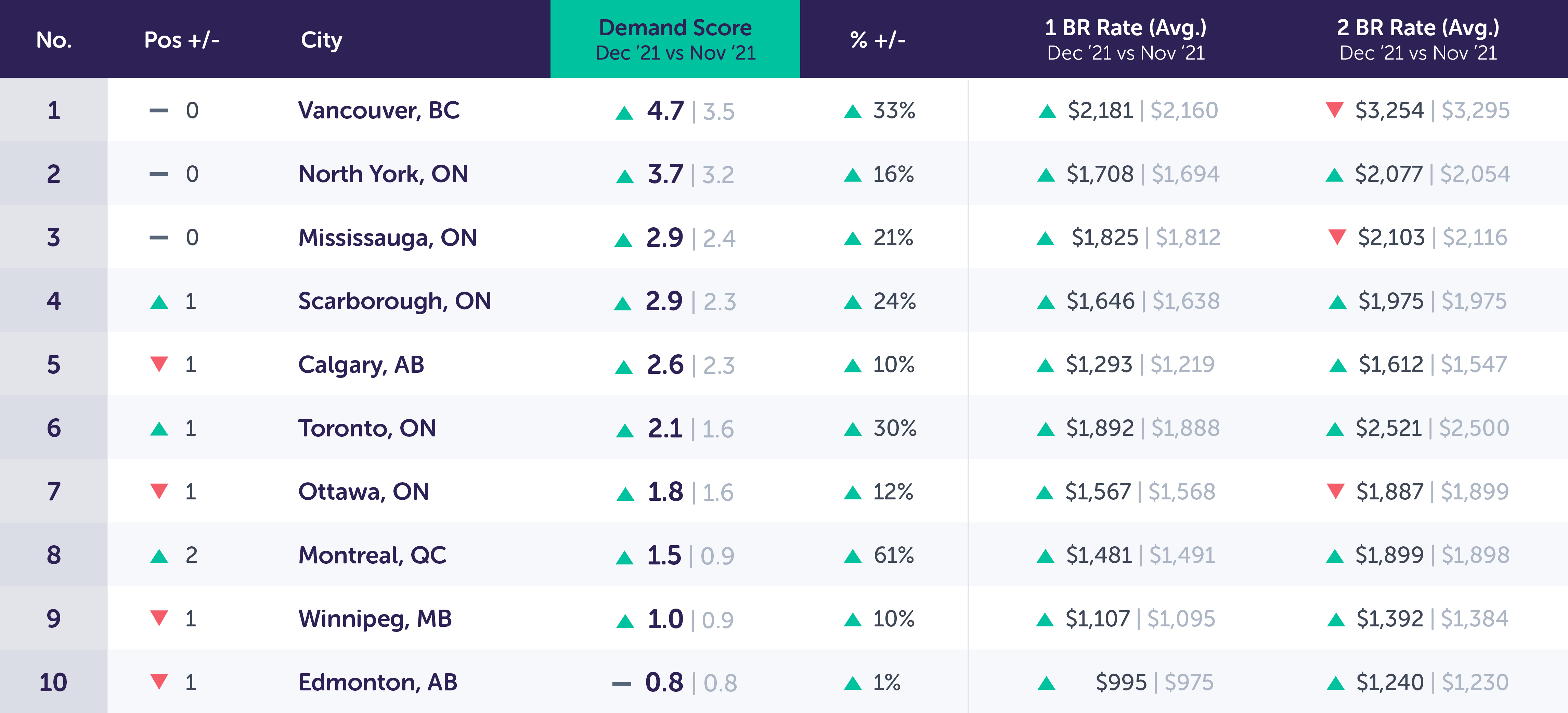

Top 10 Canadian Cities in Demand Drill Down (M/M): December 2021 vs. November 2021

Key Trends for Top 10 Canadian Cities in Demand (M/M)

*Although demand scores have maintained relatively consistent month over month, with many continuing to see upward growth, this is a result of supply shrinking at a greater rate than renter demand suggesting that seasonality has had a reduced effect on the markets overall performance, and that market fundamentals remain relatively stable month over month.

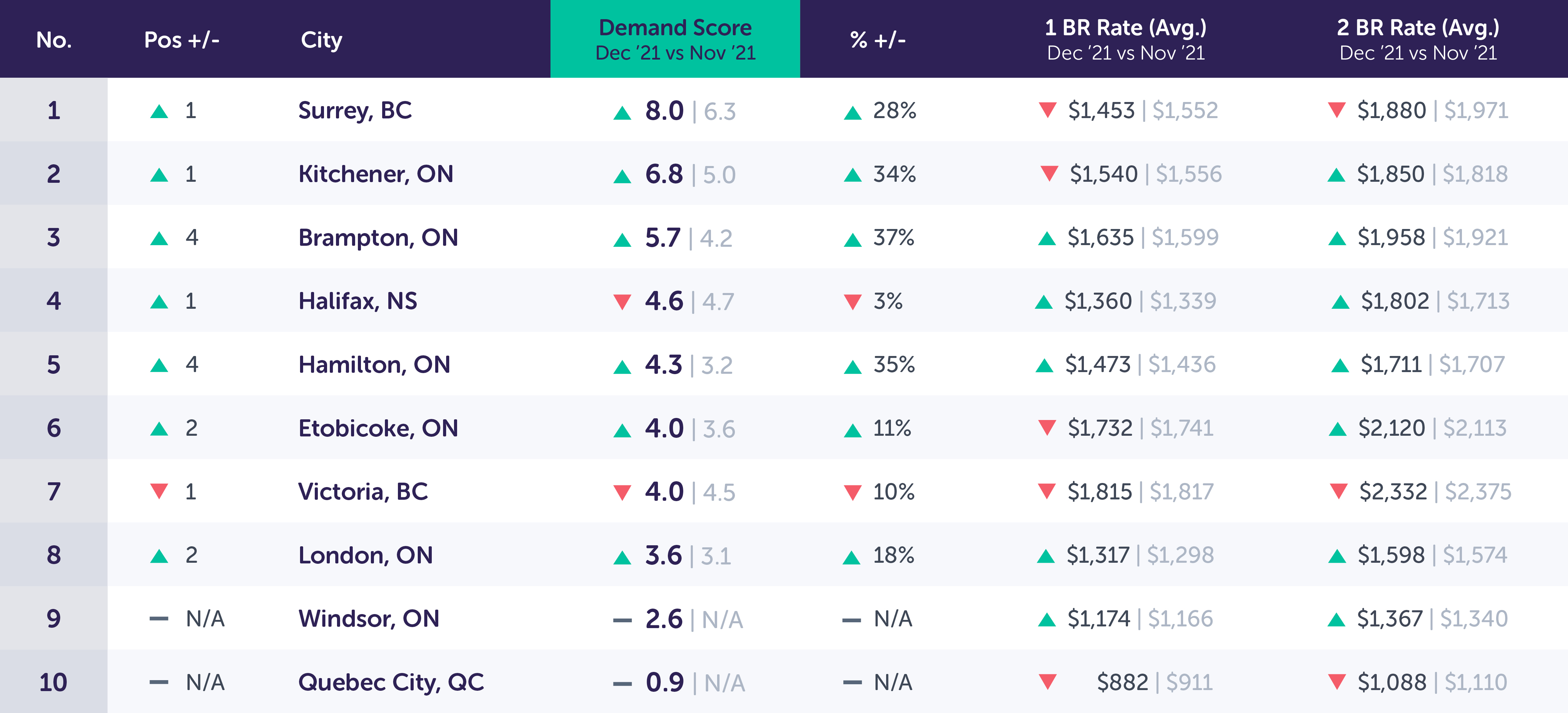

Top 10 Canadian Cities Drill Down (Y/Y): December 2021 vs. December 2020

Key Trends for the Top 10 Canadian Cities in Demand (Y/Y)

*Again we see the renormalization of renter traffic and apartment inquiries that we would expect. The markets that appear to be attracting the greatest volume of inquiries continue to be secondary markets, however, we have seen a major push for specific primary markets, namely Vacouver, and Halifax, which may be related to a more controlled COVID outbreak allowing for greater economic stability in urban centers.

In December we have seen a continuation of the trends experienced in November, however, with a further tightening supply. A greater proportion of the unoccupied units remaining from the initial covid slowdown in rental traffic are gradually reabsorbed and have caused the overall supply of listings to decrease. With many households having re-entered the rental market we have seen a reduction in online renter demand, however, this shrinkage remains lower than the decrease of available units suggesting strong continued demand as visualized by the continued growth in demand scores. Although demand trends are beginning to return to pre-COVID conditions with primary markets experiencing an increase in focus, secondary markets continue to experience the greatest relative growth in demand. Smaller outlying communities are experiencing the greatest levels of variability. Some continue to show strong growth and are likely to continue along this trend well into the future as they have cemented themselves as strong regional hubs, while others have likely already experienced peak demand and have begun to experience a reduction in relative demand.

The long term trend of individuals moving further from major markets is likely to continue across Canada, and that we are likely to see suburban communities remain in high demand, in regards to lead traffic and inquiries. Additionally, the red hot real estate market in major metropolitan areas that is also increasing rent rates, has forced many renters to consider alternative markets to find appropriate rental accommodations.

An Analysis of Key Canadian Markets

In order to better segment our data and analyze what is happening within specific markets across Canada, we have broken down our data into 3 key market segments:

- Primary (Populations Over 600K)

- Secondary (Populations Between 600-235K)

- Tertiary (Populations Between 235-100K)

Here we will gain a deeper perspective on demand across larger populations and any movement due to the impact of COVID-19 on the rental market.

Key Takeaways:

Both the supply of available units, and the demand posed by prospective renters has seen a gradual decrease; however, the relationship between the two is disparate with supply decreasing at a higher relative rate. This has enabled the overall leads per property figures to show an overall increase.

Month-Over-Month (M/M)

- Primary: Unique leads per property are up +21.7%

- Secondary: Unique leads per property are up +20.6%

- Tertiary: Unique leads per property are up +0.1%

Year-Over-Year (Y/Y)

- Primary: Unique leads per property are up +81.1%

- Secondary: Unique leads per property are up +120.9%

- Tertiary: Unique leads per property are up +49.56%

Primary Markets (Populations >600K)

Primary Market Drill Down (M/M): December 2021 vs. November 2021

Notable Changes in Primary Markets Over the Past Month

*Unique leads per property in primary markets saw an increase this month versus last month, which is likely related to a supply shortage during the month of December. Overall unique leads per property increased by 21.7% in primary markets this month.

Market fundamentals continue to return to their pre-covid states. The trend of decreasing unit availability is maintained month over month as units which have turned over, or remained vacant throughout the pandemic are being leased. Similarly, we see a continued decline in inquiries from prospective renters, which is a normal seasonal trend, while also in part due to the large number of units which were absorbed in the previous quarter. Although overall inquiries are down, average market rents continue to climb upwards and when combined with the increase in demand scores further suggests that market fundamentals remain strong and that conditions are gradually stabilizing.

(See the year-over-year analysis below, for more perspective on demand in primary markets.)

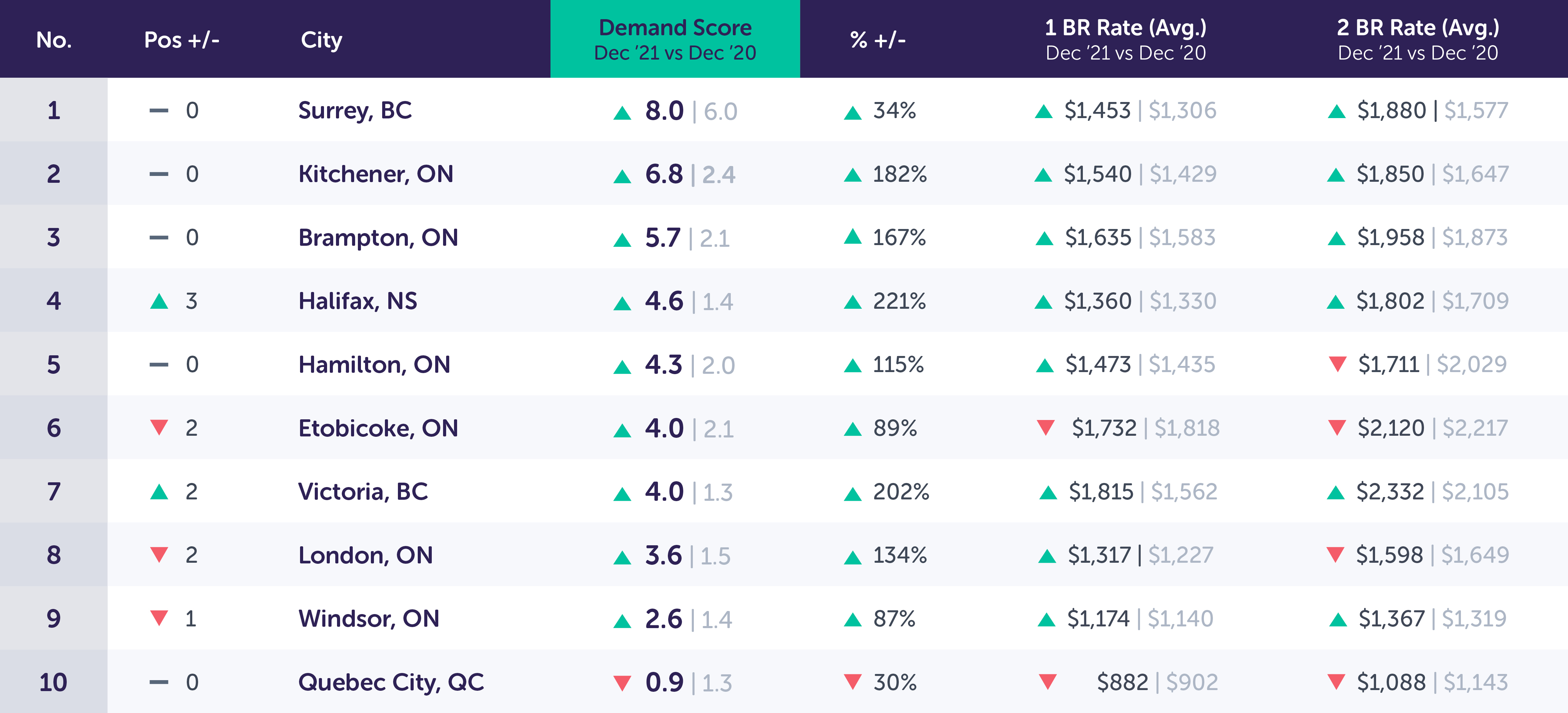

Canadian Cities – Primary Market Drill Down (Y/Y): December 2021 vs. December 2020

Notable Changes in Primary Market Demand Over the Past Year

*Overall, year-over-year primary market unique leads per property continues to rebound versus the same time last year and have increased +81.1%. Although ongoing shutdowns continue to have a negative impact on major markets the overall trend sees a return to downtown cores regardless of working conditions. For the majority of December 2021 restrictions were loosened for public gatherings, which has likely influenced a spike in lead volume compared to last year when restrictions were tighter, and vaccinations were not available. In addition to this, a shortage of rental supply has caused a spike in unique leads for properties that are currently listed.

Alongside the growing demand for apartments, we also experience growth in rental rates which suggest that not only has demand rebounded, but that market conditions are gradually returning to those experienced prior to covid and that incentives are likely to gradually disappear as competition for renters declines. This has allowed for the continued growth and acceleration of rental rates within metropolitan areas after over a year of stagnation.

Secondary Markets (Populations ~600-235K)

Secondary Markets Drill Down (M/M): December 2021 vs. November 2021

Notable Changes in Secondary Market Demand Over the Past Month

*Secondary markets saw an increase of 20.6% unique leads per property this month, an increase once again related to a shortage of supply, and continued demand for more affordable rental housing.

These communities exemplify the seasonality of rental demand much more clearly and have seen the greatest relative month over month decrease in inquiries relative to the supply of available properties. Although the relative decrease of inquiries remains lower than the reduction of available properties, this slowdown has resulted in the stagnation of achievable rents in some communities. The slowdown in rental rate growth suggests that many markets are also achieving an equilibrium compared to the previous year, where these properties experienced a large surge in demand. This has resulted in more competitive pricing as secondary markets see a stabilization of overall demand trends.

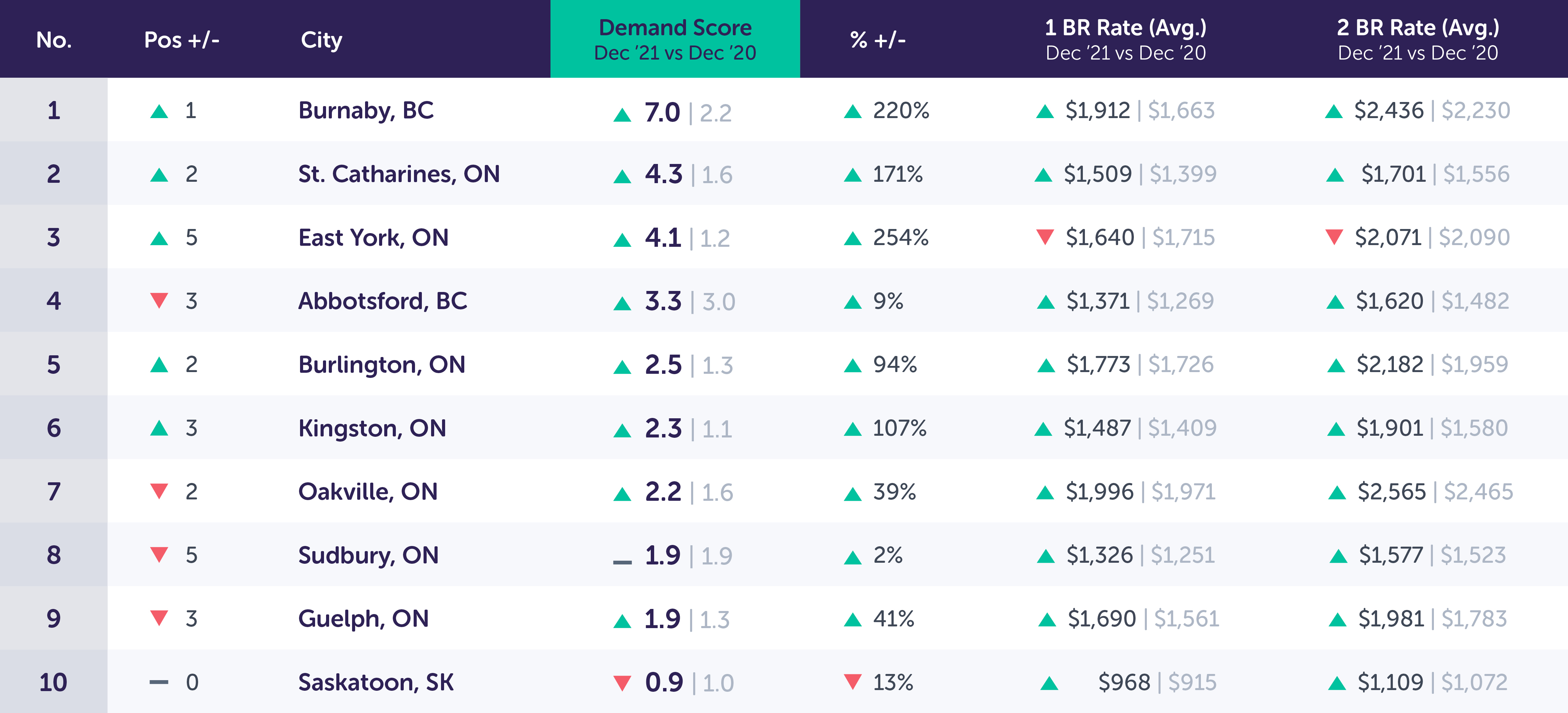

Secondary Market Drill Down (Y/Y): December 2021 vs. December 2020

Notable Changes in Secondary Market Demand Over the Past Year

*Overall, unique leads per property are up +120.9% in secondary markets this year versus this time last year. The significant year over year increase suggests that these communities are likely to continue experiencing growth in rental demand as many individuals continue to work remotely, or have simply begun to value the characteristics of secondary markets over those more urban communities.

The markets which have experienced the greatest overall levels of growth are primarily those who are not reliant on a geographically proximate major market for employment and instead contain their own business districts with sufficient employment opportunities. This has resulted in markets like Halifax, Hamilton, London, and Victoria to not only experience substantial growth in the overall demand for rental, but have also benefited from on-going rent growth. This may be an interesting trent to continue watching into the future as it suggests that these markets are likely to continue an upward trend into the foreseeable future.

Tertiary Markets (Populations ~235-100K)

Tertiary Markets Drill Down (M/M): December 2021 vs. November 2021

Notable Changes in Tertiary Market Demand Over the Past Month

*Unique leads per property increased by 0.1% this month versus last month in tertiary markets.

Tertiary markets saw the greatest level of variability regarding their month over month trends. This variability is likely to identify which markets experienced temporary growth due to covid, and which markets are likely to continue to show long term growth through their regional and local importance as economic hubs which will continue to attract renters well into the future. Regardless, both availability and demand have slowed considerably, while rental rates have experienced a similar slowdown, suggesting that many communities have begun to stabilize as they return to pre covid conditions. These communities will continue to diverge moving forward and are likely to display disparate levels of growth and associated market conditions well into the future based on broader macroeconomic conditions.

(See the year-over-year analysis below, for more perspective on the rise in demand in tertiary markets.)

Tertiary Markets Drill Down (Y/Y): December 2021 vs. December 2020

Notable Changes in Tertiary Demand Over the Past Year

*Overall, unique leads per property are up in tertiary markets +49.6% this year versus the same time last year. Year-over-year tertiary markets continue to show strong signs of growth and migration due to more affordable housing and remote work.

Although tertiary communities continue to experience gains throughout the pandemic in regards to increasing rental demand, some of this growth has receded indicating some of the appeal which had attracted many households has dissipated and many are now looking to return to larger markets. This trend is most evident in rural communities as opposed to those which are within commuting distance of a major market or offer proximate employment opportunities. Regardless, the overall trend of households' willingness to move into smaller communities persists and is likely to continue as a staple within the Canadian rental industry moving forward.

Conclusion

The data shown in this report suggests that this month the Canadian rental market has remained consistent from November to December, with minor seasonal declines in unique prospects per property. The increase in unique leads per property is unseasonal for the month of December, as we typically see a major reduction of demand during this time, but it can be concluded that as restrictions remained loose in December, and supply remained scarce, this caused a relative increase in unique prospects per property for those available on the market.

Vacancy rates in urban areas such as Toronto have dropped from 6.4% in Q1 of 2021 to 3% in Q3, and with less supply available, lead volume is becoming much more concentrated.

In fact, the year-over-year rental market comparison for vacancies in Toronto is 0.2% less from Dec. 2021 vs. Dec 2020. As homes for sale within major markets continues to tighten due to the trend of ongoing price speculation, and low interest rates, the demand for purpose-built rentals will continue to grow. With these factors in play along with slow, albeit gradual loosening of covid restrictions, we continue to see primary markets regain the moment lost during the initial phase of the pandemic. This will likely have the ultimate effect of returning us to the tight market conditions seen in some markets prior to COVID which will require a substantial investment by the development community through the construction of new product in order to alleviate.

We will continue to monitor, and provide an in-depth data analysis, month-over-month, and year-over-year to provide you with the most accurate insights that can help to support your ongoing marketing and advertising strategies, especially as we navigate through these unprecedented times.