Marketing Managers

Demand Trends for the Canadian Market:

As we delve further into the center of the summer leasing season we see demand continuing to grow alongside an increasingly more competitive rental market for those looking for a new home. Recent trends in the market remain at play with a continued decline in the available supply of properties, alongside the ever-growing number of prospective renters in the market for a new home.

After a tumultuous period of false starts and intermittent slumps, we now see just over 2 months of maintained growth in rental demand signalling that the rental market is in full swing. Demand scores are up +3.9% across our top 40 markets while tertiary markets saw the greatest gains +5.3%.

Nationally the number of prospective renters increased by +1.5%, while the number of available properties declined by -2%. Although these figures are relatively small they show a continued tightening from the previous month which saw prospective renters increase by +2.6%, and available properties decline by -1.5%. As these figures continue to move in opposite directions, the competition in the rental market amongst renters will intensify.

Renters will likely face a more challenging environment with fewer options, while property owners and managers will experience increased demand and growing rents. The implications of this trend will continue to shape the dynamics of Canada’s rental market in the coming months, impacting both renters and property owners alike.

In the following sections, we identify notable changes in rental demand, highlight market-specific trends, and discuss what the coming months may look like for the rental demand in Canada.

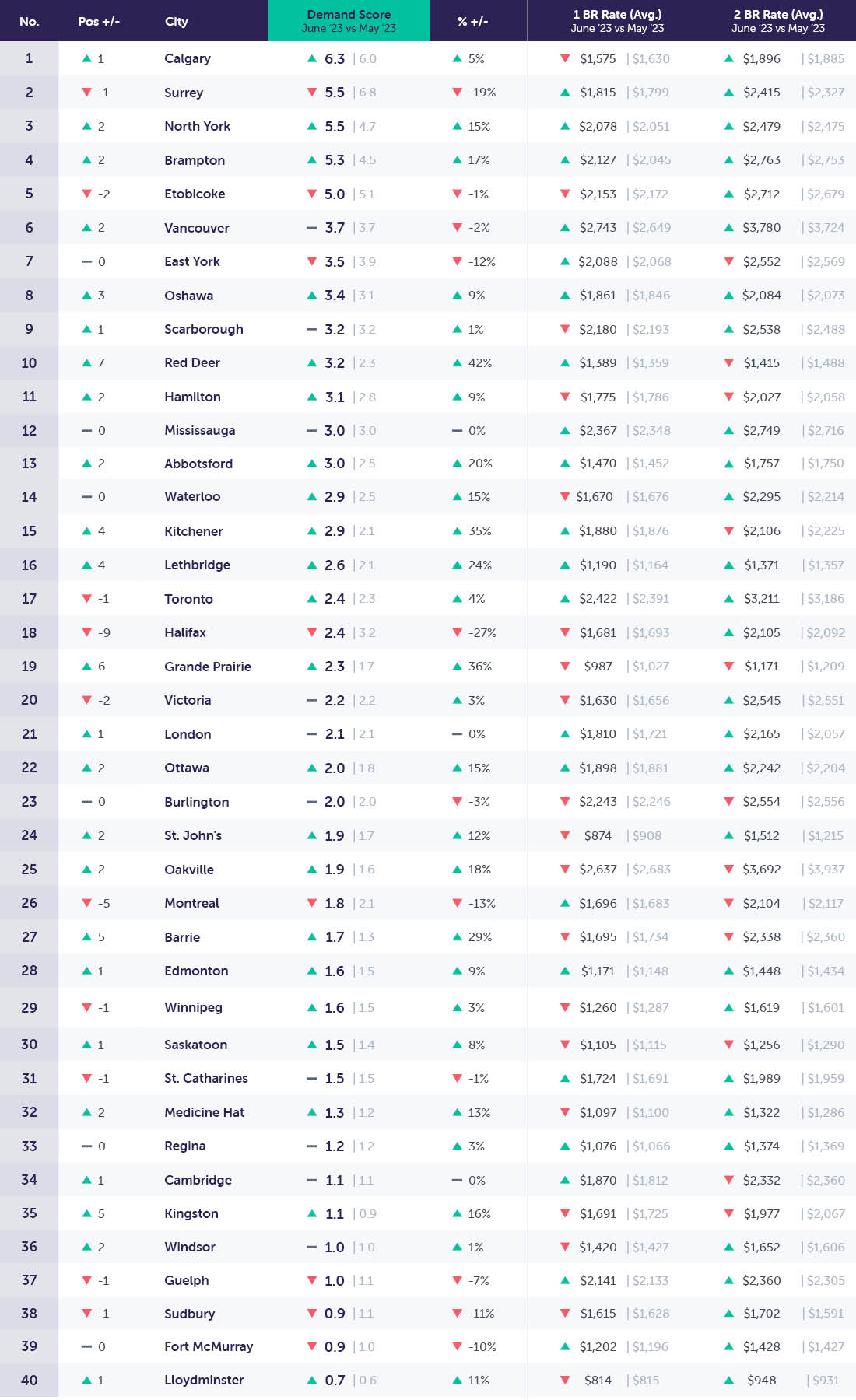

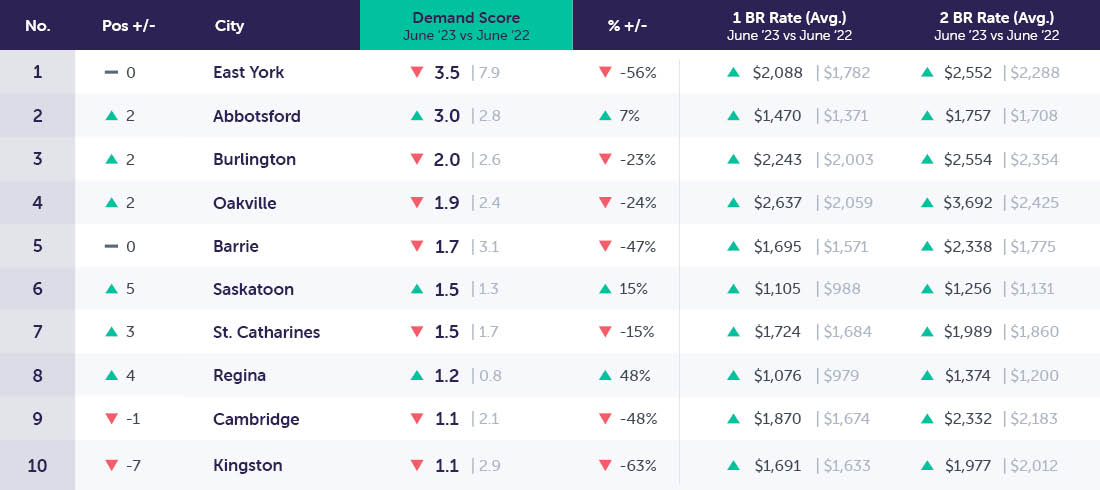

Top 40 Canadian Cities in Demand

Notable Changes in Demand Over the Past Month

Rental demand continued to grow across the country. Calgary took over the number one spot in demand rankings from Surrey. The top 10 markets as a whole saw a reshuffle after Surrey, Etobicoke, and Halifax experienced declines in rental demand. Halifax saw the greatest decline and fell 9 spots month over month due to a -30% decline in renters. Alternatively, Grand Prairie, AB saw the greatest growth in demand scores this month due in part to a decline in property availability, and a +12% increase in unique prospects thus showing that smaller markets saw the greatest growth in rental demand this month.

Month-Over-Month (M/M)

- Primary: Demand scores are up +3.6%

- Secondary: Demand scores are up +0.9%

- Tertiary: Demand scores are up +5.3%

Month-over-month (M/M) National demand scores are up +3.9% in June 2023 compared with May 2023. Continuing from May’s growth, we are now well within 2023’s summer leasing season.

Year-Over-Year (Y/Y)

- Primary: Demand scores are up +6.7%

- Secondary: Demand scores are down -32%

- Tertiary: Demand scores are down -15.4%

Year-over-year (Y/Y): National demand scores are down -4.9% in June 2023 compared with June 2022. Annual demand score comparisons have for the first time in the past year shown signs of softening with a less dramatic national year-over-year decline, and for the first time in a year annualized demand growth. 2022 saw mass return of renters to primary markets which were hampered by unleashed rental stock post-pandemic. Since then we've seen a continued decline in available rental product, alongside a growing number of prospective renters. This has resulted in a tighter rental market, and higher demand scores for those most in-demand markets.

An Analysis of Key Canadian Markets

In order to provide a more detailed analysis of the rental demand in specific markets across Canada, we have segmented our market data into 3 key market segments.

- Primary (Populations Over 600K)

- Secondary (Populations Between 235-600K)

- Tertiary (Populations Between 100-235)

Examining these market segments individually offers a deeper understanding of demand patterns within larger population centers, and allows us to identify trends across markets.

Primary Markets (Populations >600K)

Primary Market Drill Down (M/M): June 2023 vs. May 2023

Notable Changes in Primary Markets Over The Past Month

*Overall demand scores are up +3.6% month-over-month, unique prospects are up +1.8%, and properties are down -1.7%.

Primary markets saw further tightening of rental conditions with the supply and demand for rentals moving in diametrically opposite directions. With a growing population of prospective renters looking to rent from a dwindling number of available rental properties, we see no relief in sight for primary markets which represent over 73% of total renter activity across Canada.

Although as a whole property counts continue to decline, we have noticed an increase in the number of available secondary suites in single-family homes. Whether due to financial insecurity associated with higher interest rates and subsequently higher mortgage payments, or the result of greater attention being paid to the rental market as a whole by the general public. The supply of shared accommodations, and basement suites has increased thus offering more choices to renters, especially those more price sensitive and struggling to navigate the high cost of living of many larger urban markets.

Average rents continued to trend upwards in primary markets up +0.5% month-over-month, and slightly higher than the average of our top 40 markets of +0.3%. While rental demand continued to tighten, we are unlikely to see a return to the rent inflation experienced last year with 0.5% monthly rent growth as the new norm.

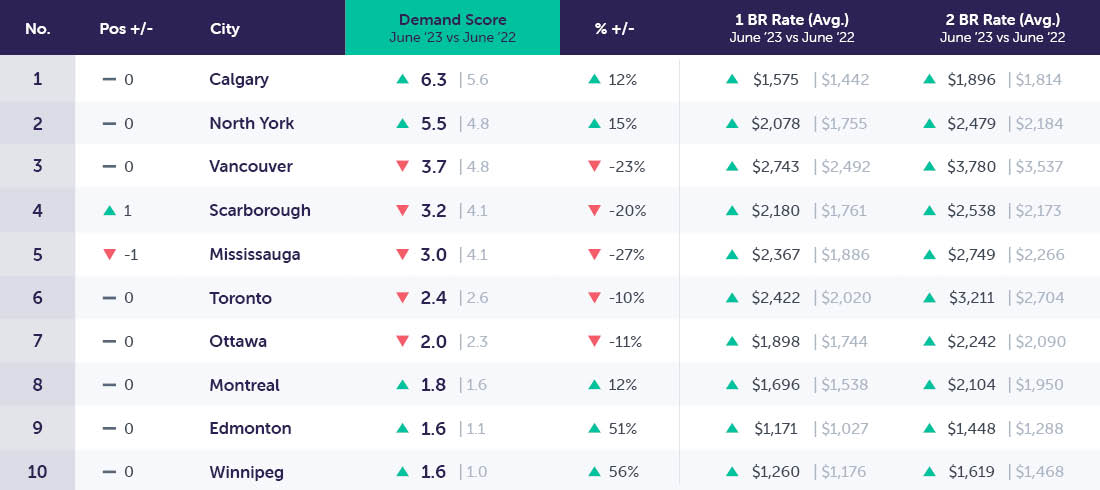

Primary Market Drill Down (Y/Y): June 2023 vs. June 2022

Notable Changes in Primary Market Demand Over The Past Year

*Year-over-year demand scores are up +6.7%, prospects are down -16%, and properties are down -21.6%

For the first time this past year, we see annualized growth in demand scores for primary markets. Although unique prospects have declined for 5 months in a row, available properties declined at an increasingly accelerated rate, resulting in higher average prospect per property counts increasing by +6.4%, and therefore higher absolute demand scores.

Having long since passed peak rental demand in 2022, we are now seeing the longer-term stabilization of market conditions, low vacancy rates, and strong renter demand. Unfortunately, the tightened market conditions have the potential to reduce demand in the short term as was seen in April, with many people opting to stay put rather than move and have to pay a higher rental rate than they can reasonably accept.

Secondary Markets (Populations ~235-600K)

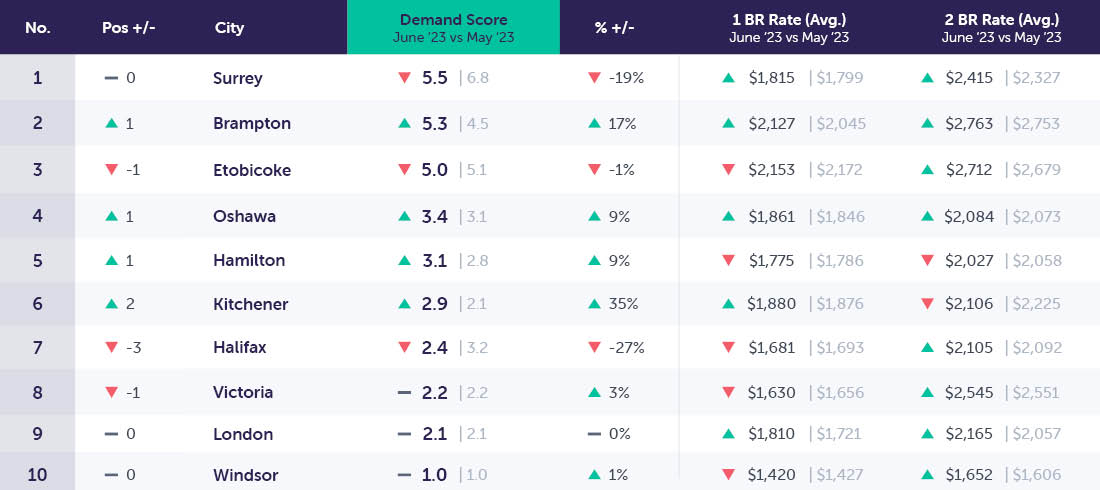

Secondary Markets Drill Down (M/M): June 2023 vs. May 2023

Notable Changes in Secondary Market Demand Over The Past Month

*Secondary markets demand scores are up +0.9% month-over-month, unique prospects are down -2.7%, and property counts are down -3.5%.

Secondary markets continue to lag behind the rest of the country. Even with declining renter counts demand remains up because property availability decreased at a faster rate. Thankfully property owners should not see this as a sign of concern as most secondary markets have maintained low vacancy rates post-pandemic. Even while many renters have moved back to their larger and better amenitized primary markets, secondary markets offer strong potential for families and those looking for a more affordable cost of living.

Although the average paints a negative impression of secondary markets, individually they offer a more varied impression of demand trends. Approximately half of our top 10 secondary markets show growth in unique prospects (Brampton, Oshawa, Hamilton, Kitchener, and Windsor) with an average of +8.8%, while the other half represents an average decline of -12%.

Secondary Market Drill Down (Y/Y): June 2023 vs. June 2022

Notable Changes in Secondary Market Demand Over the Past Year

*Overall, year-over-year demand scores are down -32% year-over-year, with prospects down by -38%, and properties down by -8.6%.

While as a whole demand scores remain down year-over-year, the number of available properties has begun to decline at an accelerated rate once again, showing that renters continue to sign leases, and properties are constantly being taken off the market.

Regardless, the current conditions experienced by secondary markets make leasing turnover units more difficult this year relative to last year. With average leads per property down -32.2% year-over-year, there are fewer renters for every available property. This leaves secondary markets more susceptible to shifts in market demand.

Property owners and managers should carefully monitor ongoing leasing trends within secondary markets in their portfolios to ensure that they are not caught off guard by any declines in lease volumes.

Tertiary Markets (Populations ~100-235K)

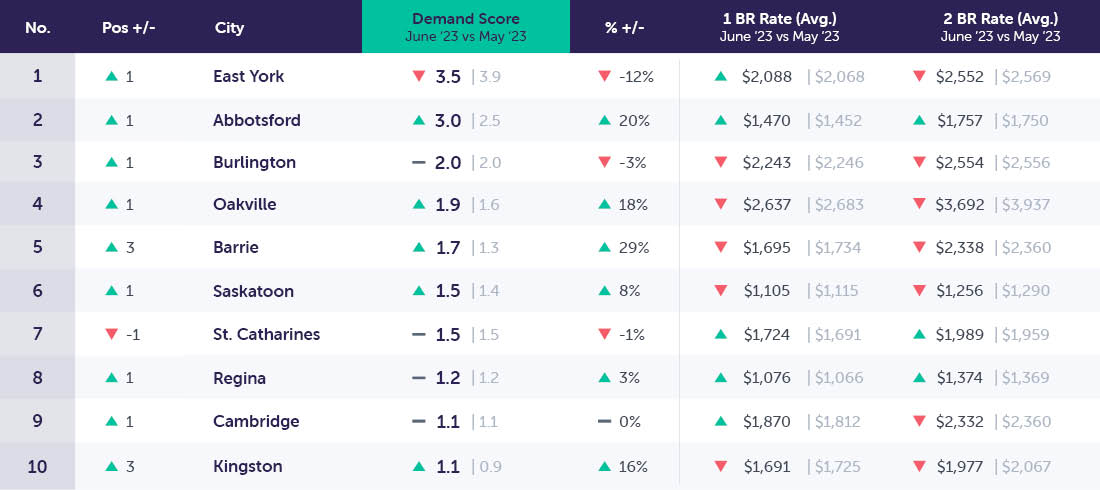

Tertiary Markets Drill Down (M/M): June 2023 vs. May 2023

Notable Changes in Tertiary Market Demand Over The Past Month

*Demand scores in tertiary markets increased by +5.3% month-over-month, unique prospects are up +2.9%, and available properties are down -2.3%.

Tertiary markets have outpaced the rest of the country with a higher-than-average increase in demand scores thanks primarily to strong growth in renter counts.

Rents remain relatively unchanged month-over-month, unlike the remainder of the country. Although this is not likely to be the reason behind the tertiary markets' recent gains in rental demand, the lower cost of living is likely to contribute to the continued and growing interest of renters within these communities.

Tertiary Markets Drill Down (Y/Y): June 2023 vs. June 2022

Notable Changes in Tertiary Demand Over the Past Year

*Overall, year-over-year demand scores are down by -15.4%, unique prospects are down by -20.1%, and available properties are down by -5.3%.

Annual comparisons have begun to show signs of recovery. While property counts are likely to continue to decline in line with the broader country, unique prospect counts have begun to show signs of recovery. Although they are unlikely to return to the pandemic highs when large swaths of renters sought tertiary markets out for their slower pace of life and increased privacy.

These communities remain appealing options for those still able to work remotely, or simply those looking for a smaller community to call home. These communities are likely to continue showing more favourable annual comparisons throughout the summer season.

Conclusion

Continuing from last month's renewed growth, June saw a continuation of trends taking us squarely into the midst of the 2023 summer leasing season. With demand for rental properties continuing to grow the rental market is becoming increasingly more competitive for those seeking new housing.

Primary and tertiary markets saw the greatest gains this month thanks primarily to a growing population of prospective renters actively searching for rental properties. Unfortunately, unless new product is brought to market to offset the constantly shrinking supply of available rental properties these communities will feel a housing pinch which will result in a resumption of uncontrolled rent growth, or simply a stalling of rental activity spurred by the financial insecurity of renter households. The outlying effects are too complex for this report however further tightening of market conditions can hurt these markets which have only just stabilized after the tumultuous period in demand that was the pandemic.

Regardless of the longstanding effects of growing rental demand, in the short term, this renewed demand offers some relief to communities that have seen demand decline over the previous 2 quarters. Many large projects which have recently come to market will benefit from growing rental demand and enable them to lease well throughout the summer.

Average market rents slowing down has similarly had an impact on renter demand. Renters see that their opportunities to get into the market before rent growth renews; are fleeting. Pushing them to make housing decisions now rather than later and motivating more renters into the market.

The renewed growth of rental demand presents a clear opportunity to property owners and managers looking to lease available units, however, it also means that the next few months will be incredibly important to ensure that their properties are well positioned leading into the cooler and slower fall and winter months. We encourage all property owners to take proactive steps towards filling vacancies and leveraging all available tools to attract quality leads to your properties.

Methodology

To present this data, Rentsync has determined three key calculations for each area of the report, they are as follows:

Demand Score: Our demand score is rated out of 10 (with 10 being the highest score a city can receive), and is calculated based on unique leads per property, per city, and compared against benchmark data.

For Example Calgary, AB received a demand score of 6.3 this month, versus 6.0 last month. Meaning Calgary experienced a 0.3-point increase in its demand score.

Demand Percentage (% +/-): This is determined according to the year-over-year (YOY) or month-over-month (MOM) increase or decrease in unique leads per property.

For Example The month-over-month demand scores in Calgary, AB went up +5% in June 2023 versus May 2023, while gaining one position within our rankings as the highest-achieving market in June. The year-over-year demand score in Calgary increased by 0.7 points representing a +12% increase from June 2022.

Position: The position is determined by unique leads per property

For Example This month, Calgary, AB achieved the top spot on our Top 40 Canadian Cities in Demand rankings and is up 6 positions from last year

*This report provides month-over-month rental listing data for June 2023 versus May 2023, as well as a year-over-year comparison from June 2023 versus June 2022. It also outlines the month-over-month and year-over-year trends in primary, secondary, and tertiary markets.