Marketing Managers

Executive Summary

In this comprehensive national rental demand report, we outline significant changes in rental market demand across Canada. The data presented here is the largest data-backed analysis of rental market demand in Canada using aggregate ILS data (over 20 rental listing sites).

The data included in the Rentsync National Rental Demand Report can be used to compare and contrast demand and lead volume for the properties you manage within a given city, and will allow you to make more sound decisions on marketing and advertising.

As you observe demand and lead volume percentage, it's possible to measure this against your own metrics, and see whether you are in line with current industry trends, and if not, how to pivot your strategies as a result.

Methodology

In order to present this data, Rentsync has determined three key calculations for each area of the report, they are as follows:

Demand Score: Our demand score is rated out of 10 (with 10 being the highest score a city can receive), and is calculated based on unique prospects, per property, per city, and compared against benchmark data from the past 12 months.

For example: Oshawa, ON received a demand score of 5.7 this month, versus 6.3 last month. Therefore, Oshawa experienced an decrease in demand (unique prospects per property) by 0.6 points this month.

Unique Prospects Percentage (% +/-): This is determined according to the year-over-year (YOY) or month-over-month (MOM) increase or decrease (aka the demand) in unique prospects per property / per city.

For example: The month-over-month unique prospects in Oshawa, ON went down 10% in February versus January. However, in February 2021, the year-over-year unique prospects in Oshawa, ON went up 60% compared to January 2020.

Position: The position is determined by unique prospects per property, with cities that have at least *20 properties or more. Position will vary depending on demand.

For example: This month, Oshawa remained in the #1 spot on the Top 50 Canadian Cities in Demand despite a slight decrease in month-over-month prospects per property (-10%), which could be attributed to the shorter month, and less cumulative days to collect prospect data (minus 3 days). Whereas Abbotsford, BC moved up 2 spots (from 5th to 3rd on the list), despite maintaining its demand score from last month.

*The following report provides month-over-month ILS data for February 2021 versus January 2021, as well as a year-over-year comparison from February 2021 versus February 2020. It also outlines the month-over-month and year-over-year trends in primary, secondary, and tertiary markets.

Key Takeaways:

Month-over-month (M/M): Overall, total unique prospects from January to February decreased -7.5%, and number of available properties decreased -1.8%, however, this data was collected during a 28-day month versus a 31-day month, therefore the overall decline in unique prospects per property is likely attributed to this, and not necessarily attributed to a significant reduction in demand.

This month each market saw a relative decrease in unique prospects per property: Primary (-12.3%), Secondary (-10%), and Tertiary (-1.3%).

Interestingly, unique prospects per property in Secondary and Tertiary markets have toppled Primary. There are nearly double, +49.3% unique prospects per property in Secondary markets, and +34.7% unique prospects per property in Tertiary markets versus Primary this month.

*Overall, many Canadian cities will have experienced a decrease in demand from February 2021 versus January 2021, based on the reduced number of days in the month, and also due to government enforced lockdowns for the majority of February.

Year-over-year (Y/Y): Overall demand for multifamily rental housing is actually up +8.9% this year, versus the same time last year, however, supply is also up +30.7% with more than 2,862 new properties entering the long-term rental market this year versus the same time last year. Therefore, supply is outpacing demand nearly 3x this year versus last.

Primary markets are down (-35.6%), secondary markets are down (-21%), and tertiary markets are down (-25.2%) this year versus last year. It is worth noting that last year February 2020 had an additional day for data collection, which may be impacting the data. However, it is still clear that the pandemic has affected rental housing demand year-over-year, and lockdown measures throughout the winter months are causing many to postpone their rental housing search. As vaccines continue to roll out throughout the year, a surge in demand is likely to occur in later months.

Additionally, increased supply has impacted unique prospects per property across the majority of Canadian cities year-over-year. As more supply floods the market (i.e. Airbnbs), demand is being spread out.

We can hypothesize that this downward trend may begin to reach its final threshold as more people are vaccinated, and as travel and, schools, and restrictions begin to loosen. However, for the time being, we can expect COVID-19 to continue to impact migration away from urban city centers to locations with more space and more affordable housing, as remote work continues to increase.

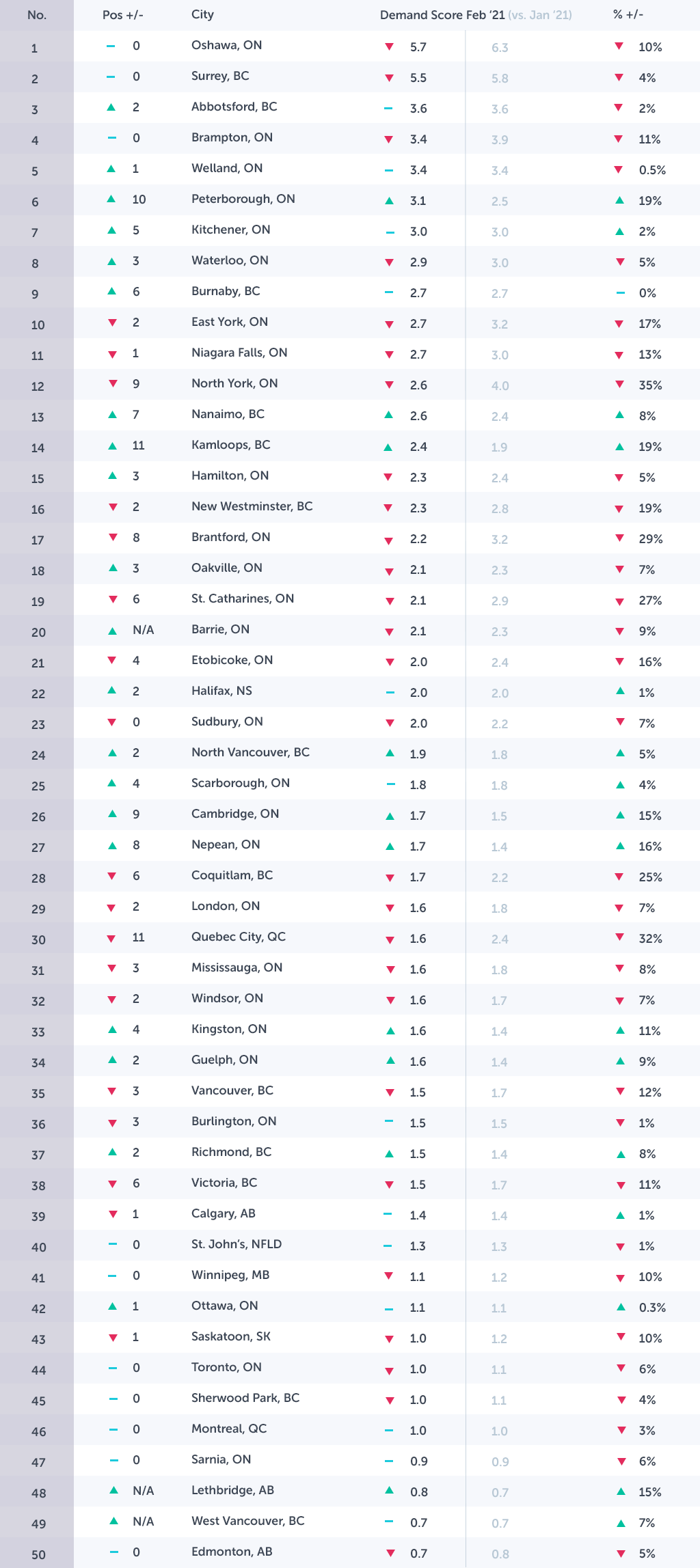

Top 50 Canadian Cities in Rental Demand

*Demand is calculated using unique prospects per property per city for Feb 2021 versus Jan 2021

Notable Changes in Demand Over the Past Month

- Overall, the majority of Canadian cities experienced a minor decline in demand this month, with only a few experiencing any significant upwards or downwards trends. This is likely attributed to the shorter month (28 days), and therefore, 3 less days to convert prospects versus the previous month.

Upwards

- Peterborough, ON moved up 10 spots, increased demand by +0.6 and experienced a +19% increase in prospects per property.

- Nanaimo, BC moved up 7 spots, and saw an increase in demand of +0.2, and an +8% increase in unique prospects per property.

- Kamloops, BC moved up 11 spots, and saw an increase in demand of +0.5 points, and a +19% increase in unique prospects per property.

- North Vancouver, BC moved up 2 spots, and saw an increase in demand points of +0.1, and a +5% increase in unique prospects per property.

- Cambridge, ON moved up 9 spots, and saw an increase in demand of +0.2 points, and a +15% increase in unique prospects per property.

- Nepean, ON moved up 8 spots, and saw an increase in demand points of +0.3, and a +16% increase in unique prospects per property.

- Kingston, ON moved up 4 spots, and saw an increase in demand points of +0.2, and a +11% increase in unique prospects per property.

- Guelph, ON moved up 2 spots, and saw a +0.2 increase in demand points, and a +9% increase in unique prospects per property.

- Lethbridge, AB entered the top 50 list, increasing demand by +0.1 points, and unique prospects per property by +15%.

No Demand Change

- Abbotsford, BC moved up 2 spots this month, but remained at 3.6 on the demand scale, and saw a -2% decrease in unique prospects per property.

- Welland, ON moved up 1 spot overall, remained steady at 3.4 demand points, but saw a slight -0.5% decline in unique prospects per property.

- Kitchener, ON moved up 5 spots on the list, but remained at 3.0 demand points, and experienced an increase of +2% in unique prospects per property.

- Burnaby, BC moved up 6 spots, remained at 2.7 points on the demand scale, and had no change in unique prospects per property.

- Halifax, NS moved up 2 spots, but remained at 2.0 points in demand, and saw a +1% increase in unique prospects per property.

- Scarborough, ON moved up 4 spots, remaining at 1.8 demand points, and a +4% increase in unique prospects per property.

- Burlington, ON moved down 3 spots, but remained at 1.5 demand points, and saw a -1% decrease in unique prospects per property.

- Calgary, AB moved down 1 spot, but remained at 1.4 on the demand scale, and increased +1% in unique prospects per property.

- St. John's, NFLD remained in 40th position, remaining at 1.3 demand points, and a decrease of -1% in prospects per property.

- Ottawa, ON moved up 1 spot this month, remained at 1.1 in demand points, and saw a slight +0.3% increase in demand.

- Montreal, QC remained at 46 on the top 50 list, and at 1.0 demand points, and experienced a decrease of -3% in demand.

- Sarnia, ON remained in 47th position, and 0.9 demand points, and saw a -0.6% decrease in unique prospects per property.

- West Vancouver, BC entered the top 50 list at the 49th position, remaining at 0.7 in demand points, but increased unique prospects per property by +7%.

Downwards

- North York, ON moved down 2 spots, saw a -0.6 decline in demand points, and a -35% decrease in unique prospects per property this month.

- Brantford, ON moved down 8 spots, and reduced demand by -1.0 points, experiencing a drop of -29% in unique prospects per property.

- St. Catharines, ON moved down 6 spots this month, reduced demand by -0.8 points, and saw a -27% decrease in unique prospects per property.

- Etobicoke, ON moved down 4 spots, reduced demand by -0.4 points, and saw a -16% decrease in unique prospects per property.

- Coquitlam, BC moved down 6 spots, saw a -0.5 reduction in demand points, and a -25% decrease in unique prospects per property.

- Quebec City, QC moved down 11 points this month, and saw a -0.8 decrease in demand points, with a -32% decrease in unique prospects per property.

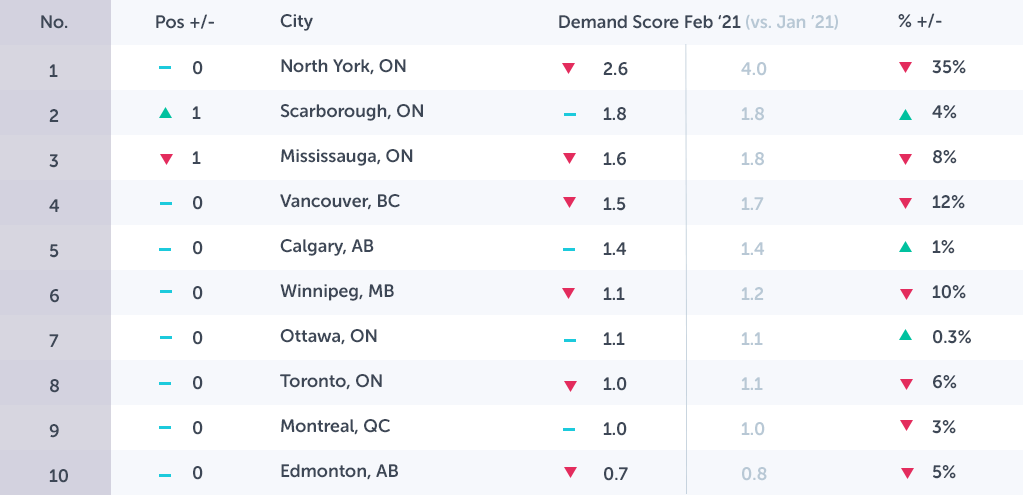

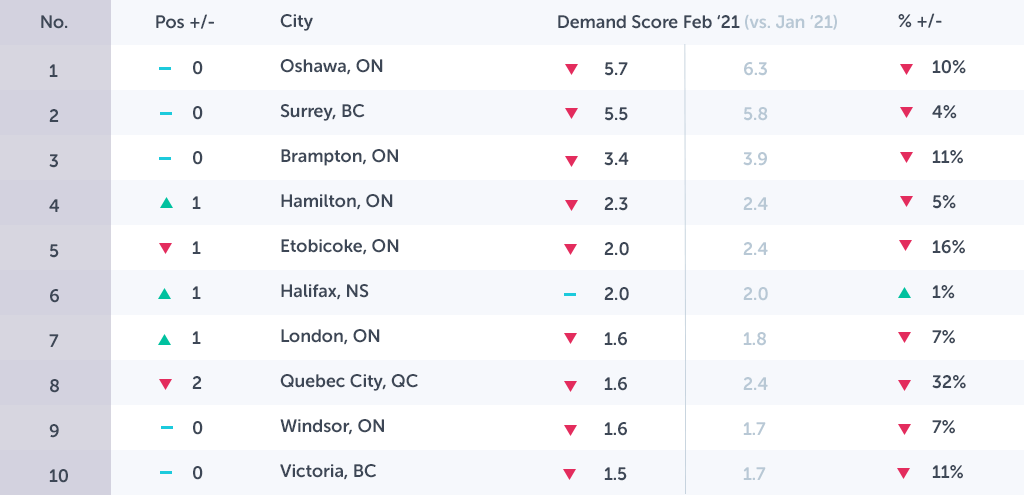

Top 10 Canadian Cities in Demand Drill Down (M/M): Feb 2021 vs. Jan 2021

Key Trends for Top 10 Canadian Cities in Demand (M/M)

- Oshawa, ON took the top spot again this month, despite a decrease of -0.6 in demand points, and a decrease of -10% in unique prospects per property.

- Surrey, BC remained in the 2nd spot, and saw demand decrease by -0.3 points, with a slight -4% decrease in unique prospects per property.

- Abbotsford, BC moved up 2 spots, remained at 3.6 demand points, and saw a -2% decrease in unique prospects per property for the month.

- Brampton, ON stayed in 4th position, spots on the list, and saw a -0.5 decrease in demand points, and a -11% decrease in unique prospects per property for the month.

- Welland, ON moved up 1 spot this month, remained at 1.5 demand points, and slightly decreased unique prospects per property by -0.5%.

- Peterborough, ON moved up 10 spots, increased demand by +0.6 points, and unique prospects per property by +19%.

- Kitchener, ON moved up 5 spots this month, remaining at 3.0 demand points, and a +2% increase in unique prospects for the month.

- Waterloo, ON moved up 3 spots, despite experiencing a -0.1 decrease in demand points and -5% decrease in unique prospects per property.

- Burnaby, BC moved up 6 spots, remaining at 2.7 demand points, experiencing no change in unique prospects per property.

- East York, ON moved down 2 spots on the list, and saw a decrease in demand points by -0.5, and -17% decrease in unique prospects per property.

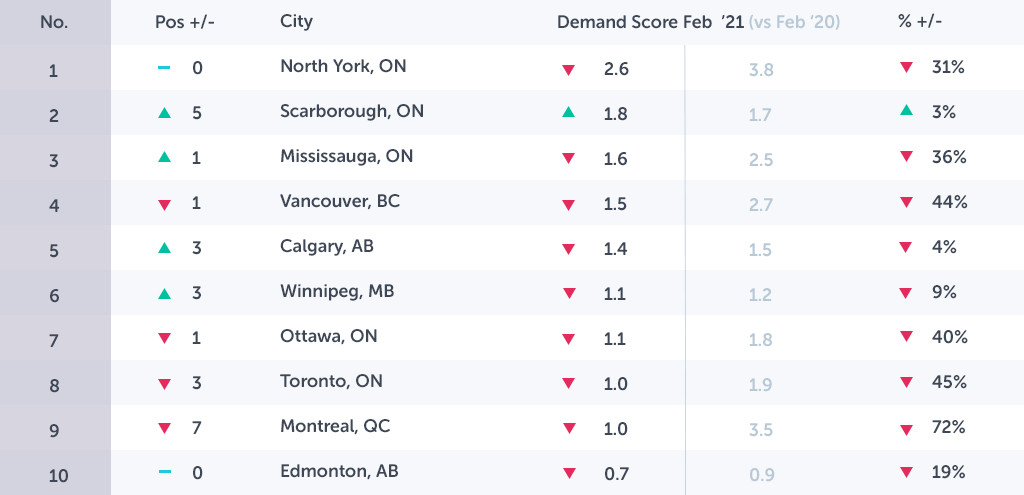

Top 10 Canadian Cities Drill Down (Y/Y): Feb 2021 vs. Feb 2020

Key Trends for the Top 10 Canadian Cities in Demand (Y/Y)

*Note: It is worth mentioning that last year was a leap year, and February had an additional day in the month, and therefore should be accounted for when observing this data.

- Oshawa, ON moved up 28 spots from this time last year, and increased demand by +3.1 points, and increased 60% year-over-year in unique prospects per property.

- Surrey, BC moved down 1 spot this year, and decreased demand by -+5.0 points, and experienced an decrease of -45% in unique prospects per property this year versus the same time last year.

- Abbotsford, ON moved up 20 spots this year, increasing demand points by +1.0, and saw a +27% increase in unique prospects per property.

- Brampton, ON moved down 1 position from last year, but saw a decreased demand of -2.4 points, and a -41% decrease in unique prospects per property.

- Welland, ON moved up 4 spots this year, but decreased demand by -0.3 points versus this time last year, and saw a decrease of -8% in unique prospects per property.

- Peterborough, ON moved up 5 spots, but decreased demand by -0.5 points, and saw a decrease in unique prospects per property by -11%.

- Kitchener, ON moved down 1 spot, decreased demand by -1.5 points, and decreased unique prospects per property by -32% this year versus last year this time.

- Waterloo, ON moved down 3 spots on the list, and saw demand decrease of -1.8 points, and -39% unique prospects per property.

- Burnaby, BC moved down 2 spots, and saw demand decrease by -1.1 points, with a decrease of -29% in unique prospects per property.

- East York, ON moved down 6 spots, seeing a reduced demand of -2.0 points, and a decrease of -43% unique prospects per property versus the same time last year.

*It appears the increase in demand found in Oshawa, ON, and Abbotsford, BC, continue to be related to remote work and migration to less densely populated areas with reduced rent rates and larger living space. The decline in areas such as Welland, ON (-8%) and Peterborough, ON (-13%) are likely related to the shorter month, and appear to be on par from last year.

An Analysis of Key Canadian Markets

In order to better segment our data and analyze what is happening within specific markets across Canada, we have broken down our data into 3 key markets:

- Primary (Populations Over 600K)

- Secondary (Populations Between 600-235K)

- Tertiary (Populations Between 235-175K).

Here we will gain a deeper perspective on demand across larger populations, and any movement due to the impact of COVID-19 on the rental market.

Primary Markets (Populations >600K)

Canadian Cities – Primary Market Drill Down (M/M): Feb 2021 vs. Jan 2021

Notable Changes in Primary Markets Over the Past Month

*Demand in primary markets decreased this month versus last month. Overall, supply experienced no change in primary markets, however, demand decreased by -12.3% this month versus last month.

Upward

*No primary markets experienced any significant increase in demand this month versus last month

No Change in Demand

- Scarborough, ON remained at 1.8 demand points and experienced a +4% increase in unique prospects per property this month.

- Calgary, AB remained at 1.4 demand points, and saw a 1% bump in unique prospects per property.

- Ottawa, ON remained at 1.1 demand points, and saw a slight +0.3% in unique prospects per property.

- Montreal, QC stayed at 1.0 demand points and experienced a slight decline (-3%) in unique prospects per property.

- Edmonton, AB decreased demand points by -+0.1 and experienced a -5% decrease in unique prospects per property.

Downward

- North York, ON decreased demand points by -1.4 and -35% in unique prospects per property this month versus last.

- Mississauga, ON decreased by -0.2 demand points, and saw a decrease of -8% unique prospects per property this month.

- Vancouver, BC experienced a decrease of -0.2 demand points and a -12% decrease in unique prospects per property this month.

- Winnipeg, MB saw a slight -0.1 decrease in demand points and a -10% decrease in unique prospects per property this month.

- Toronto, ON experienced a slight decrease of -0.1 in demand points and a -6% decrease in unique prospects per property.

*Overall, month-over-month demand in primary markets from January to February were overall stable, except for North York, ON (-35% in unique prospects per property), who experienced a strong start to 2021, and was likely due to a marketing and advertising push in January. Overall, however, primary markets are indicating that it may be reaching its bottom, as rent rates have decreased throughout 2020 and into 2021. We may begin to see primary markets reemerge in later months as vaccines become more widespread and borders and travel reopens.

(See the year-over-year analysis below, for more perspective on demand in primary markets.)

Canadian Cities – Primary Market Drill Down (Y/Y): Feb 2021 vs. Feb 2020

Notable Changes in Primary Market Demand Over the Past Year

*Overall, total unique prospects per property decreased -35.6% year-over-year in primary markets, while listings for rental properties are up 36% this year versus the same time last year in primary markets.

*Due to increased vacancies/availability, supply is outpacing demand in the majority of primary markets this year versus the same time last year.

Upward

- Scarborough, ON has experienced a slight increase in demand points (+0.1) from this time last year and has moved up 5 spots in primary markets, and an increase of +3% in unique prospects per property year-over-year.

Downward

- North York, ON remained at the top of the primary market list, but decreased demand by -1.2 points, and saw a decrease of -31% in unique prospects per property.

- Mississauga, ON had a -0.9 point decrease in demand points, and a -36% decline in unique prospects per property.

- Vancouver, BC experienced a -1.2 decrease in demand points and a -44% decrease in unique prospects per property year-over-year.

- Calgary, AB moved up 3 spots from this time last year, however, saw a slight -0.1 decline in demand points, and -4% in unique prospects per property.

- Winnipeg, MB also moved up 3 spots from this time last year, and saw a -0.1 decrease in demand points, and -9% decline in unique prospects per property.

- Ottawa, ON decreased by -0.7 in demand points, and saw a -40% decline in unique prospects per property from last year.

- Toronto, ON decreased demand by -0.9 points and saw a -45% decline in unique prospects per property.

- Montreal, QC reduced demand by -2.5 points, and has seen a drastic decline of -72% in unique prospects per property.

- Edmonton, ON saw a -0.2 decrease in demand points, and a -19% decline in unique prospects per property.

*Certain primary cities such as Calgary, AB, Winnipeg, MB, and Edmonton, AB continue to be less impacted by the effects of COVID-19 on year-over-year demand due to less affected populations and spacious more affordable rental housing conditions. Scarborough, ON is beginning to see some return to normal rental market conditions despite COVID-19.

*However, major metros such as Toronto, ON and Montreal, QC continue to see fluctuating case numbers related to COVID-19, therefore it is not surprising that cities in these regions continue to see a downward trend in demand. Given that many workers have migrated away from these areas for the foreseeable future, a sudden resurgence in demand is unlikely until borders and travel reopens.

Secondary Markets (Populations ~600-235K)

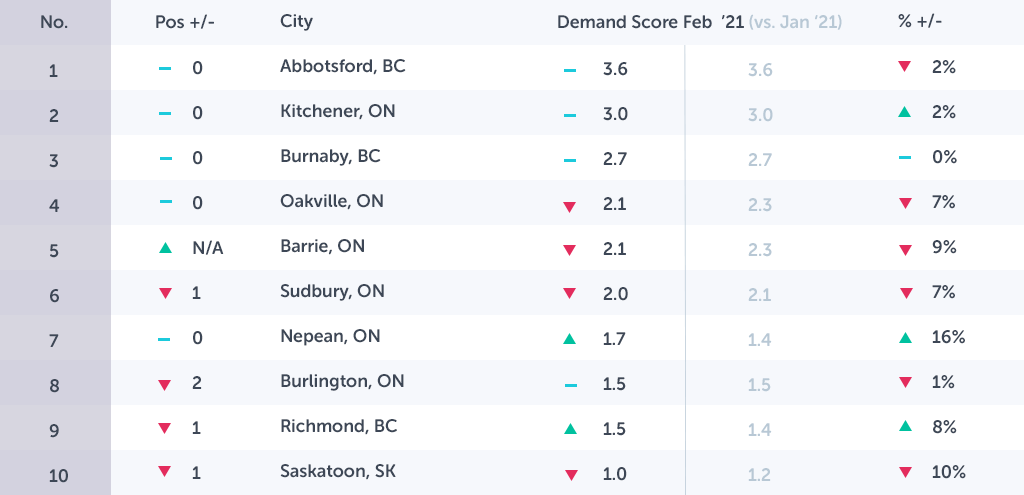

Canadian Cities – Secondary Markets Drill Down (M/M): Feb 2021 vs. Jan 2021

Notable Changes in Secondary Market Demand Over the Past Month

*After a strong start to the year, secondary markets saw a decrease of -10% in demand this month, with supply shrinking by -3.5% in these areas. However, given the short month, secondary markets are still positioned for strong month-over-month demand, with a question of whether supply will be able to offset continued demand.

No Demand Change

- Halifax, NS remained at 2.0 demand points and saw an increase of +1% unique prospects per property versus last month.

Downward

- Oshawa, ON decreased demand by -0.6 points this month and has seen an decrease of -10% in unique prospects per property this month versus last.

- Surrey, BC decreased demand by -0.3 demand points, and a -4% decline in unique prospects per property.

- Brampton, ON saw a decrease of -0.5 in demand points, and a -11% decrease in unique prospects per property this month.

- Hamilton, ON experienced a slight decrease of -0.1 in demand points and a -5% decrease in unique prospects per property this month versus last.

- Etobicoke, ON saw a -0.4 decrease in demand points, and a -16% decrease in unique prospects per property.

- London, ON reported a -0.2 decrease in demand points and a -7% decrease in unique prospects per property this month versus last month.

- Quebec City, QC experienced a decrease of -0.8 in demand points and a decrease of -32% in unique prospects per property this month.

- Windsor, ON experienced a slight decrease of -0.1 demand points, and a -7% decrease in unique prospects per property this month.

- Victoria, BC saw a decrease of -0.2 in demand points, and a -11% decrease in unique prospects per property.

Canadian Cities – Secondary Market Drill Down (Y/Y): Feb 2021 vs. Feb 2020

Notable Changes in Secondary Market Demand Over the Past Year

*Overall, total unique prospects per property are down -21% in secondary markets this year, and supply is up +24.4% in secondary markets this year versus this time last year.

Upward

- Oshawa, ON increased demand by +3.4 demand points and +60% unique prospects per property this year versus last year.

- Victoria, BC experienced a +0.2 increase in demand points and +10% increase in unique prospects per property this year versus the same period last year.

No Demand Change

- Windsor, ON remained at 1.6 in demand points, and saw a slight -1% decrease in unique prospects per property versus this time last year.

Downward

- Surrey, BC decreased in demand by -5.5 points and had a -45% decline in unique prospects per property this year versus this time last year.

- Brampton, ON decreased in demand by -2.4 points, and saw a decline in unique prospects per property by -41% this year versus last.

- Hamilton, ON decreased in demand by -1.2 points this year and experienced a -35% decline in unique prospects per property this year versus this time last year.

- Etobicoke, ON demand decreased in demand by -0.7 points and saw a -25% decline in unique prospects per property.

- Halifax, NS saw a -1.1 point decrease in demand and a -35% decrease in unique prospects per property

- London, ON decreased its demand score by -0.3 points and saw a -13% decrease in unique prospects per property this year versus the same time last year.

- Quebec City, QC experienced a decline of -0.7 in demand points and a -30% in unique prospects per property.

*Again, this month is 1-day shorter compared to last year, making the year-over-year decline in unique prospects per property appear larger. We will see a more accurate year-over-year depiction of secondary markets in next month's report.

Tertiary Markets (Populations ~235-175K)

Canadian Cities – Tertiary Markets Drill Down (M/M): Feb 2021 vs. Jan 2021

Notable Changes in Tertiary Market Demand Over the Past Month

*Overall, tertiary markets are extremely stable right now, and are seeing little to no change in demand month-over-month.

*Unique prospects per property decreased by -1.3% this month versus last month in tertiary markets, with a decrease of -1.9% in rental supply in these areas month-over-month.

(See the year-over-year analysis below, for more perspective on the rise in demand in tertiary markets.)

Upward

- Nepean, ON increased demand by +0.3 points and saw an increase of +16% in unique prospects per property this month.

- Richmond, BC experienced a +0.1 increase in demand points and an +8% increase in unique prospects per property this month.

No Demand Change

- Abbotsford, BC remained at 3.6 in demand points, and saw a slight -2% decline in unique prospects per property this month versus last month.

- Kitchener, ON stayed at 3.0 in demand points this month and experienced a +2% increase in unique prospects per property.

- Burnaby, BC remained at 2.7 demand points, and saw no change in unique prospects per property.

- Burlington, ON went up +0.2 in demand points, and saw a 14% increase in unique prospects per property.

Downward

- Oakville, ON reduced demand by -0.2 points this month versus last month and experienced a -7% decrease in unique prospects per property.

- Barrie, ON experienced a -0.2 decline in demand points, and a -9% decrease in unique prospects per property.

- Sudbury, ON saw a slight -0.1 decrease in demand points and a -7% decrease in unique prospects per property this month versus last month.

- Saskatoon, SK also decreased demand by -0.2 points and decreased by -10% in unique prospects per property this month.

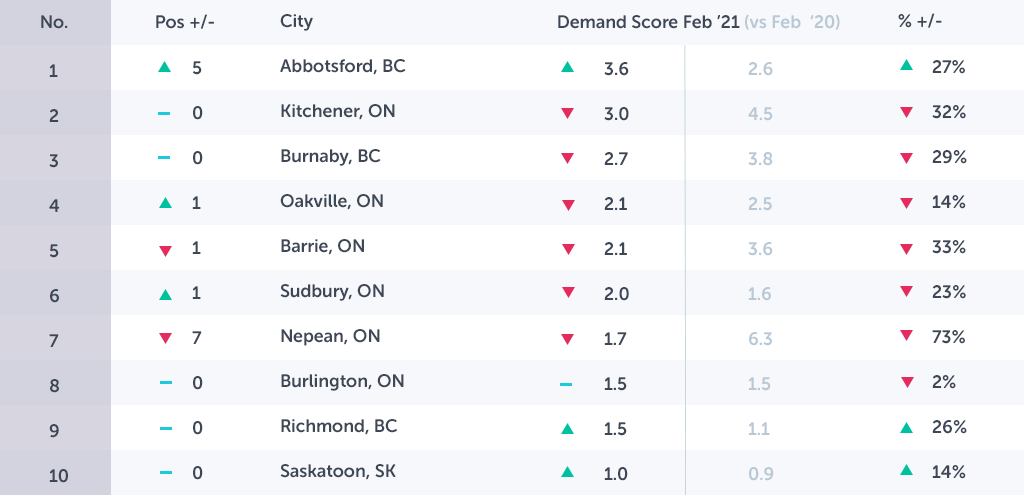

Canadian Cities – Tertiary Markets Drill Down (Y/Y): Feb 2021 vs. Feb 2020

Notable Changes in Tertiary Demand Over the Past Year

*Due to a shorter month, along with COVID-19 related lockdowns, and an increase in supply in certain areas, some tertiary markets are seeing weakened demand in February. However, others are showing growth in demand this year versus last year.

*Overall, total unique prospects per property are down -25.2% this year versus the same time last year, and number of properties are up +20.2% this year versus the same time last year.

Upward

- Abbotsford, BC saw a +1.0 point increase in demand this year, and a +27% increase in prospects per property versus last year.

- Sudbury, ON saw a +0.6 point increase in demand as well as a +23% increase in unique prospects per property this year versus the same time last year.

- Richmond, BC went up +0.4 demand points and +26% in unique prospects per property this year versus this time last year.

- Saskatoon, SK increased its demand by +0.1 points and unique prospects per property by +14% this year versus the same time last year.

No Demand Change

- Burlington, ON remained at -1.5 demand points, and saw a slight -2% decrease in unique prospects per property this year versus this time last year.

Downward

- Kitchener, ON decreased demand by -1.5 points and unique prospects per property by -32% this year versus last year.

- Burnaby, BC decreased demand by -1.1 points and -29% unique prospects per property from this time last year.

- Oakville, ON experienced a -0.4 decrease in demand points, and a -14% decrease in unique prospects per property.

- Nepean, ON experienced a -4.6 point decline in demand, and a -73% decrease in unique prospects per property versus this time last year.

Conclusion

The data shown in this report shows that rental market demand has remained relatively stable in many Primary, Secondary, and Tertiary, cities month-over-month, and is showing normal shifts in demand due to the impact of COVID-19 shutdowns, in addition to February 2021 being a short month for measuring volume.

Additionally, there are notable year-over-year changes in demand in certain markets. Primary markets continue to indicate declining demand, where secondary and tertiary markets show relative stability year-over-year, and in some cases extreme growth, due to migration away from city centers. Areas with lower population and more affordable housing are seeing the greatest increase in demand.

We will continue to monitor, and provide an in-depth data analysis, month-over-month, and year-over-year to provide you with the most accurate insights that can help to support your ongoing marketing and advertising strategies, especially as we navigate through these unprecedented times.